Why invest in China?

This piece expands on themes discussed in our recent Why Invest? podcast: Exploring the opportunity in China.

China remains one of the most polarising equity markets with the narrative swinging between “unstoppable” and “uninvestable”.

China has delivered extraordinary economic growth, and yet equity returns there have disappointed over the long-term. We think that is because profitability typically competed away when supply expands faster than demand - a feature of China’s economy. High savings feed the SOE-led banking system, which in turn provides abundant, low‑cost capital into industries. This is often amplified by state-directed capital allocation and investment decisions, which weakens the “invisible hand” that normally curbs overinvestment and declining returns; capacity can keep expanding even when economics deteriorate.

The lesson for us as investors in Asia, is that demand growth, in isolation, is not enough. Without industry rationality and resilient profitability, long-term shareholder returns are unlikely to be attractive.

Given that, we believe long‑term winners in Asia and China tend to be found where either: (i) industries are already concentrated and disciplined, or (ii) supply is improving because weaker competitors are exiting or consolidating.

We discuss this supply side framework further in our 2024 piece on China - “the reports of my death have been greatly exaggerated”.

To bring this to life in the podcast we give the example of portfolio holding H World, China’s leading hotel chain.

H World is growing its hotel portfolio through an asset-light franchise model. This allows for high rates of growth at extremely high incremental rates of return. This is made possible by H World’s scale and platform advantages, including its enormous membership ecosystem (of over 300m members), well-regarded brands, and procurement cost advantages. H World has also shown a discipline in returning its profits to shareholders via buybacks/dividends, rather than using it to build additional hotels that China does not need.

Governance

We also discuss the importance of governance within our process, and the nuances of this in China. In China, shareholder interests can be subordinated when a business’ activities conflict with political priorities (for-profit education is the classic example), and interventions can be swift and value destructive. Our risk management approach is to avoid areas of the market where the government is either explicitly present (such as through SOEs) or has a vested interest in promoting its political interests above others. As a further support to alignment, we prioritise investing in owner‑operator businesses where management has meaningful equity and incentives to protect and grow per‑share value through disciplined capital allocation.

Technology, AI & R&D

Global investors often see AI through a US lens, which is characterised by enormous capital intensity, leading-edge GPUs, and closed source Large Language Models. China is following a different course. That is partly due to constraints on its access to leading edge chips, but also for ideological reasons - to create self-sufficiency and reduce reliance on US-led tech hardware supply chains. That has meant that China’s AI roll-out has been substantially less capital intensive, only incurring c.20% of the capital deployment of the US thus far. To overcome those restrictions, Chinese open-source model developers have made innovative and creative designs (such as the Mixture of Experts architecture used by Deepseek), to allow Chinese open-source models to operate with comparable performance to their US peers.

We also discuss how China’s AI roll, and broader industrial complex, benefits from its substantial investment in power generation, energy storage and transmission. China added roughly 370GW of renewable capacity in 2024 (vs 58GW in the US). They have also invested heavily in energy storage, helping drive battery costs down ~75% over the last 5 years, and expanded grid transmission by adding 8,200 miles of ultra‑high voltage over the last 5 years versus ~375 miles in the US. That helps solve for both energy cost and energy availability.

Our conclusion is that China should benefit from substantial supply of cheap “inference” availability, allowing firms to roll out AI at low cost, consistent with the government’s “AI+” targets for widespread industrial integration of AI. That will benefit companies at the application-layer, that can use AI to strengthen their competitive position.

We discuss on the podcast how Tencent will be a key beneficiary of this AI roll out, given that its WeChat super app is an end-to-end consumer ecosystem, with 1.3bn habitual users and enormous proprietary data.

We discuss these points further in our recent article “Made in Ch-AI-na”.

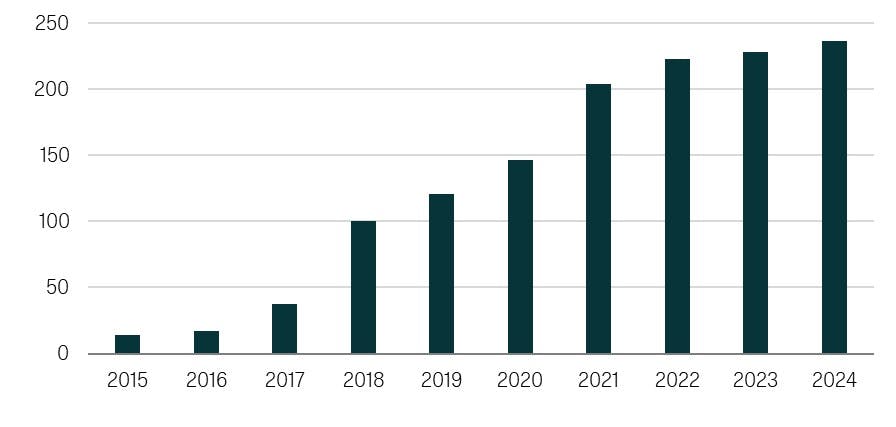

The podcast also discusses China’s broader R&D evolution, with making global investors waking up to China’s capability, and in many cases dominance, across various technology areas. This has not happened overnight, but instead reflects a decade of increased focus and investment into R&D and human capital. China now produces 3.5m STEM graduates per year vs 0.8m per year in the US – while its public companies have also dramatically increased their investments in R&D.

Chinese Equities total R&D spending (US$bn)

Source: Factset

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may rise as well as fall, and investors may not get back the amount originally invested. Capital security is not guaranteed.

This material is provided for informational purposes only and does not constitute investment advice or a recommendation. It should not be considered an offer to buy or sell any financial instrument or security. Any investment should be made based on a full understanding of the relevant documentation, including a private placement memorandum or offering documents where applicable.