What does the Budget mean for your investment strategy?

Budget

The recent UK budget has seen both taxes and government spending increase significantly; this has contrasted with last year’s stated aims of the Chancellor to reform welfare spending and not to increase tax thresholds. Labour Party MPs have, perhaps, forced a more Rayner-esque approach on Rachel Reeves. So, even with the pandemic in recent memory, the UK is seeing higher taxes on “working people”, and on employers, while the welfare bill is rising significantly after the Prime Minister and Chancellor failed to get their MPs to back modest cuts. As a result, The Office of Budget Responsibility (OBR) has downgraded its growth expectations for the rest of this parliament; this is consistent with the despondent mood of British businesses which have been shedding jobs in response to higher minimum wage and national insurance costs. It is not just businesses which are feeling the pinch but wage costs impact, of course, all employers including hospices, churches, care homes and GP surgeries. In addition to this, we are seeing a significant “brain drain”; not just billionaires are leaving.

Growth

For investors wanting to see election promises about going for growth materialise, there is little about which to get excited. The UK and large western European peers face strong competition from the US and emerging markets while being relatively expensive and highly regulated markets.

- Global competition is intensifying: Europe also has to deal with the rapid development of and growing competition from China, India and other emerging markets while lagging the largest developed market’s performance. The US economy has delivered far superior growth compared to Europe this century (and last) which leaves the average American earning around $86k while the average German or British worker makes around $30k less; Europeans on average wages maybe don’t realise that their American counterparts are paid 35%+ a year more than them. Large European democracies have good intentions, no doubt, with their higher taxation and welfare availability than the US but are not so good at making a bigger GDP cake to share nationally, perhaps. Maybe higher taxation deters investment. Higher welfare availability potentially distorts labour markets. Whatever the reasons for European growth lagging the US, it does not seem that the UK, Germany, France or Italy are moving towards their more “capitalist” model.

- Energy policy continues to give UK industry and homes very high costs relative to peers; this hits investment plans, production and the consumer. While subsidising the purchase of electric cars mostly made elsewhere, UK car production is at a multi decade low.

- Attracting foreign capital: The UK has seen the loss significant capital investment projects to other countries with more business friendly taxation systems. London remains a leading global financial centre but faces competition from around the world as well as “AI” impacting service sectors.

- National debt levels are high in the UK, post pandemic, and set to grow. We are promised deficits may be smaller which means the total national debt still grows over this parliament. If inflation falls and interest rates (bond yields) decline, the approximately £100bn annual interest cost facing UK taxpayers can ease. But if growth is lower than hoped and if there is any inflation shock, that interest bill can grow painfully. Currently, the UK borrows around £150bn p.a. while paying two thirds of that away to cover existing debt interest; perhaps not a great inheritance to pass on to future taxpayers. Having said that, the UK fiscal situation may be improving more quickly that G7 peers.

- More positively, Global economic performance remains robust; it is important to keep the bigger picture and context in mind. GDP growth may be sluggish in the UK, Germany and other parts of the world, but we are not in recession. Interest rates are expected to fall here and in the US. Companies are expected to improve their earnings in all regions globally in the next few years.

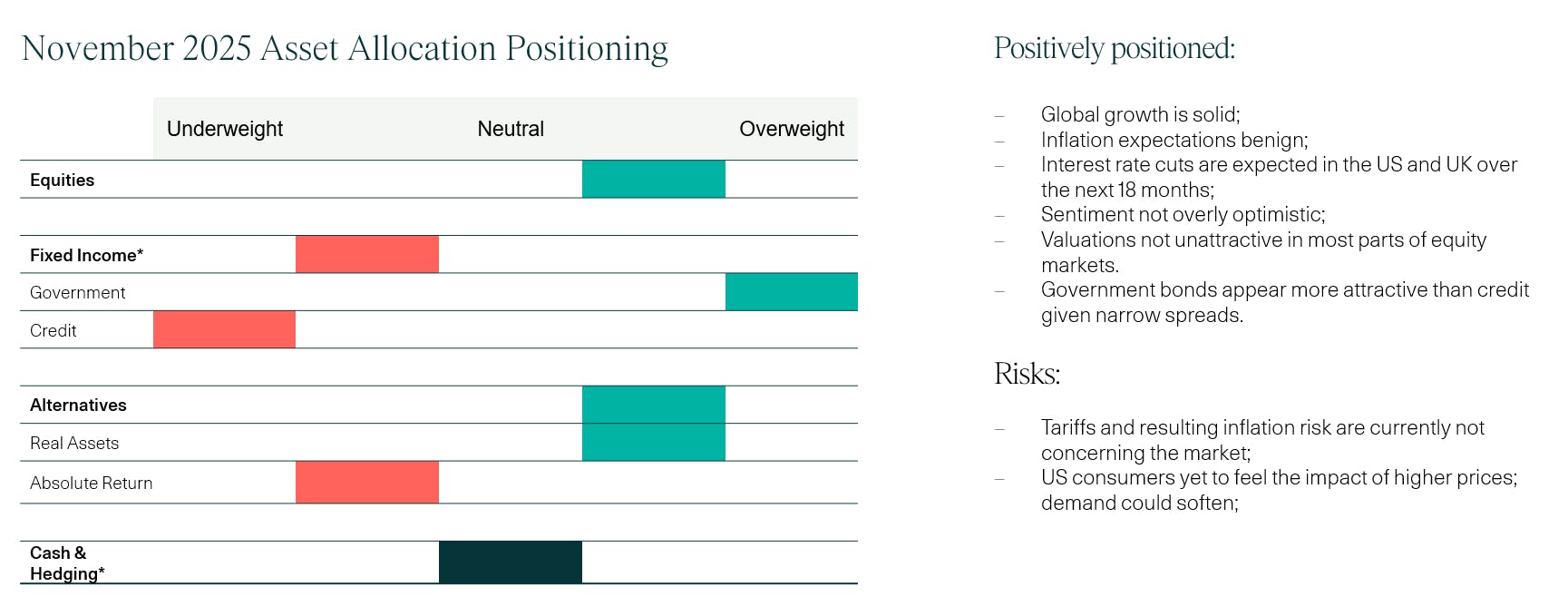

- The first thing to say about the budget and investment strategy is, be global; the opportunity set we have is bigger than just the UK. At the asset allocation level, we remain positively positioned in our chosen equity exposures, encouraged by a positive global earnings growth outlook.

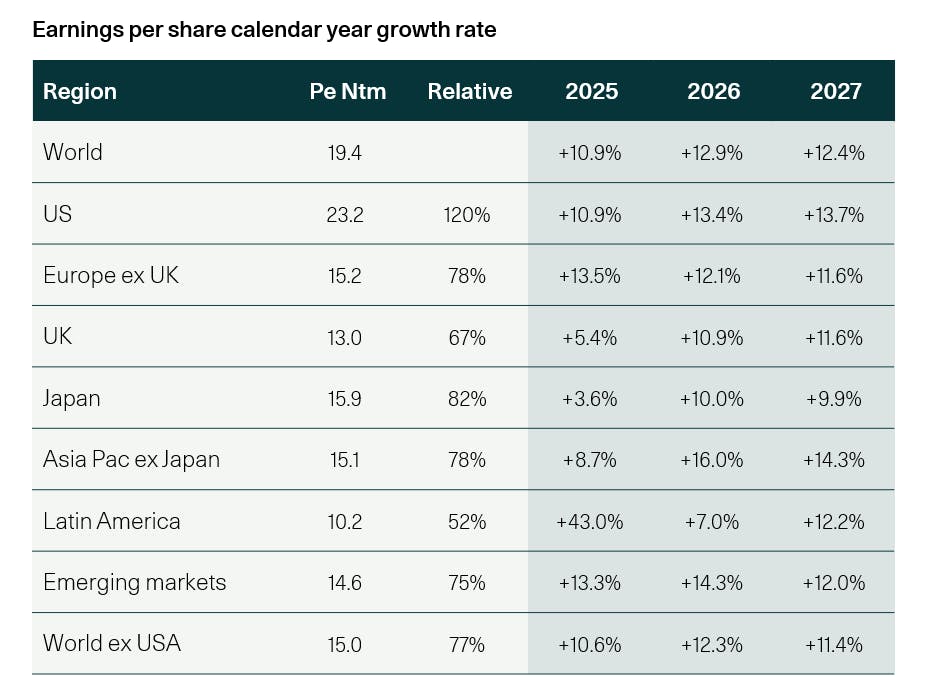

2025 earnings growth estimate +11%

+11% globally and +11% for the US

For 2025, the consensus numbers have come down from earlier in the year when 14% growth was expected in the US and 13% in the World index but the 11% and 11% expected for 2025 is still robust and there remains confidence about strong growth in the out-years too.

Despite the good earnings reports that we have generally seen in early Q3 reporting, there remains great uncertainty about the impact of tariffs.

It remains the case that there are valuation excesses in some of the leading companies in the US but valuations in the rest of the US market, and in the rest of the world, are not stretched as the first and second columns of numbers in the following table show.

Source: MSCI, FactSet, W1M. Data as at 30.09.25

Secondly, being active and direct allows us to find many good ideas both in the UK and around the world. We have written recently about how we select stocks globally and find many very interesting ideas. At W1M, our research team finds many interesting ideas with strong prospects, on a three year or longer time horizon, all over the world. The US may have a more pro-business government than the UK but we are able to find investment opportunities both there and here.

How do we find opportunities?

Seeking to identify companies where the market underappreciates the quality of the business

Source: W1M, Google Images.

Risk warning: This allocation should be used as a guide only. Differing market conditions may mean the above weightings will decrease or increase tactically. The investments listed are for example purposes and should not be considered as advice or a sollicitation to buy or an offer to sell a security.

Inflation

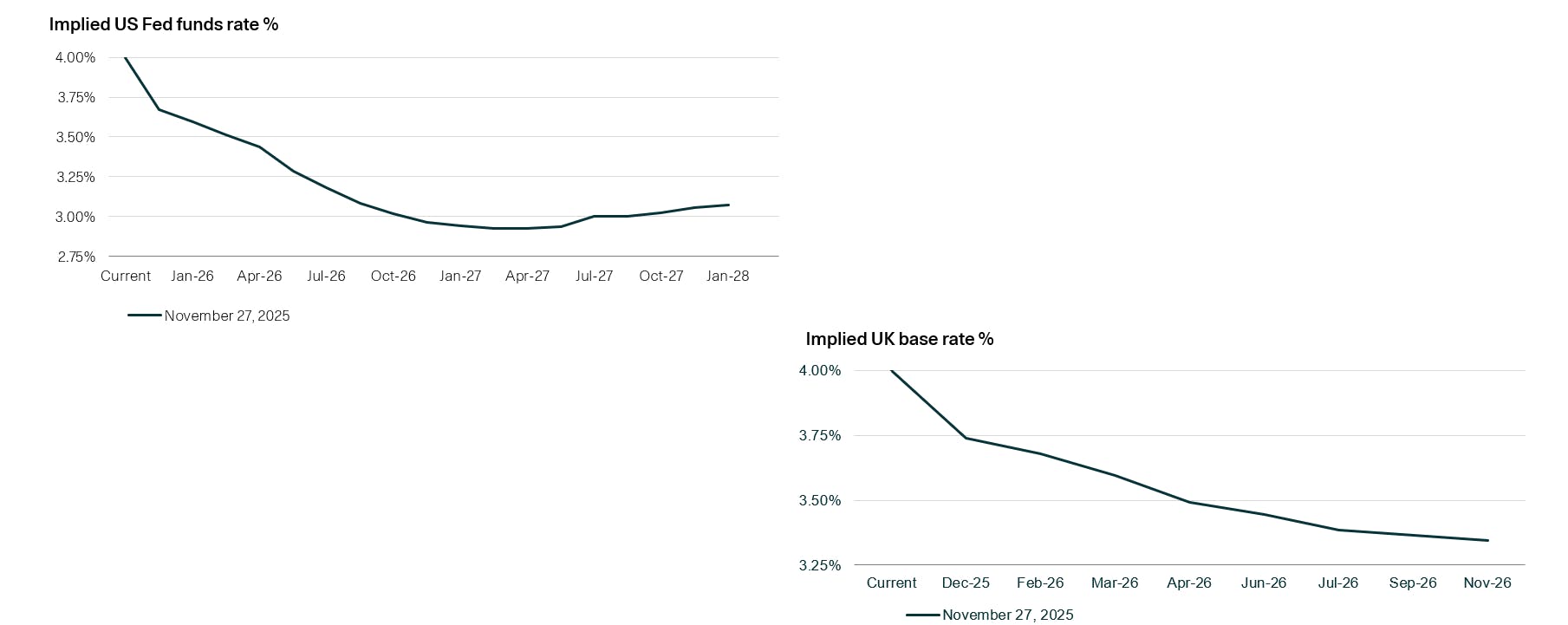

Thirdly, while weaker growth may not be welcomed by most of us, it can be a positive for gilts (government bonds) if it means inflation is not as strong as it might be and the Bank of England could have a chance to cut interest rates more than currently expected. A record high tax burden is in the end a type of austerity for those impacted; it might dampen consumption and investment plans. The UK labour market is already under massive pressure; even the US is seeing weaker job creation now. If weaker labour markets reduce inflationary pressures, the bond market can benefit. As inflation is generally expected to go down, central banks are expected to be able to cut interest rates and that means bond prices can go up. Having a preference for gilts (UK government bonds) over credit (company issued debt) in our diversified solutions currently could therefore benefit from weaker UK growth now predicted by the OBR if we see, as consensus expects, lower inflation numbers over the next year.

Expectations for future inflation remain anchored

Source: Bloomberg, W1M. As at 27.11.25

Rate cuts expected in the US an UK

Source: Bloomberg, W1M. As at 21.11.25

Real assets & absolute return strategies

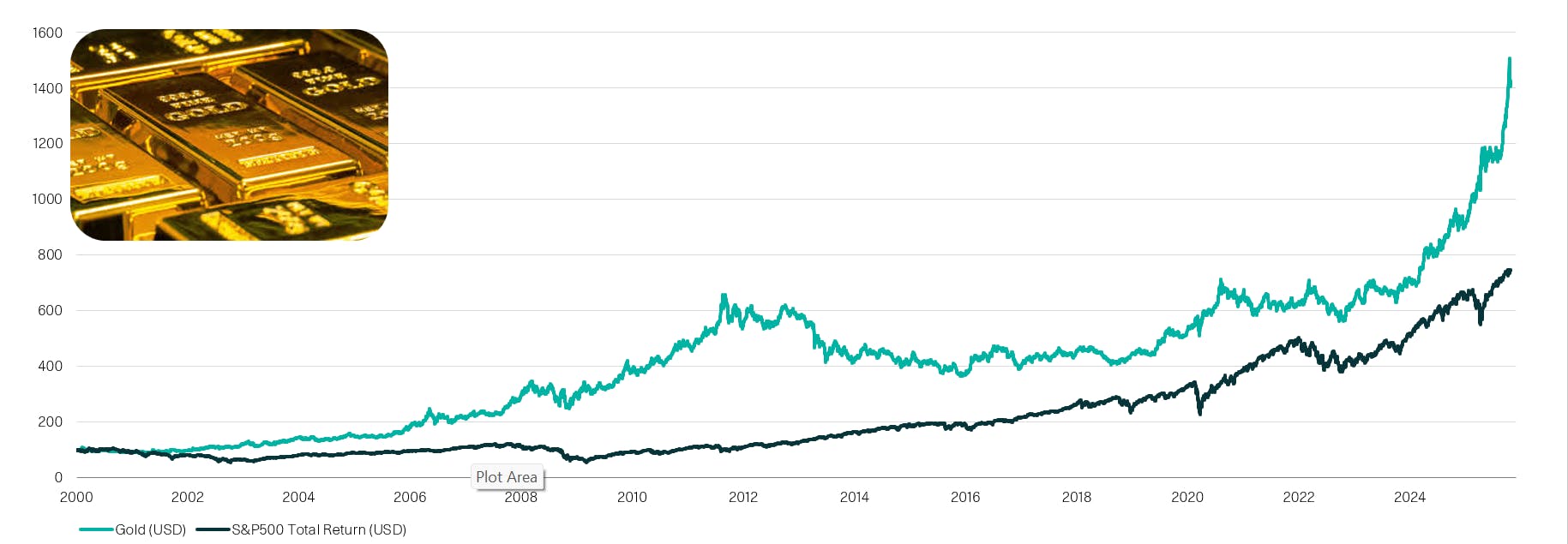

Fourthly, while we see a global macro picture with positive earnings growth across regions and the prospect of interest rate cuts in the US and elsewhere, given some concern in markets regarding “AI bubbles” and ongoing tariff war impacts maybe yet to be felt by consumers and in inflation numbers, we diversify with much more than just equities and bonds. Including real assets in portfolios (such as gold, copper, uranium, property) adds both greater diversification, upside potential and a greater degree of inflation resilience to portfolios.

Real Assets and Absolute Return strategies can provide uncorrelated protection against equity risks

Gold has recovered strongly in the 21st Century

Source: Bloomberg, Waverton. Data as of 24.10.25

Risk warning: The information above is for example purposes only and should not be considered a sollicitation to buy or an offer to sell a security. Iti based on our current view of the markets and is subject to change. Past performance is no guarantee of future results and the value and income from such investments and their strategies may fall as well as rise. You may not get back you initial investment. Capital security is not guaranteed.

Summary of our views

November 2025 Asset Allocation Positioning

*The table shows bond allocations relative to bond composite index

**Hedging includes gold & Protection Strategy if possible. Data as at 31.12.2024

Risk warning: The above should be used as a guide only. It is based on our current view of markets and is subject to change. As at 24.09.25

The W1M Investment Barometer – November 2025

In summary, it is undeniable that all the major economies have to think seriously about how to deal with their long term growth rates, spending, debt, taxation and regulation issues in an increasingly competitive world, but we are not in a UK or global recession. Consensus expects inflation to fall and interest rates to be cut in the next year. Being global, well diversified and active gives investors a wide opportunity set with which to seek consistent returns over the medium to longer run.

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may rise as well as fall, and investors may not get back the amount originally invested. Capital security is not guaranteed.

This material is provided for informational purposes only and does not constitute investment advice or a recommendation. It should not be considered an offer to buy or sell any financial instrument or security. Any investment should be made based on a full understanding of the relevant documentation, including a private placement memorandum or offering documents where applicable. W1M Wealth Management Limited is authorised and regulated by both by the Financial Conduct Authority of 12 Endeavour Square, London E20 1JN, with firm reference number 120776 and the U.S. Securities and Exchange Commission of 100 F Street, NE Washington, DC 20549, with firm reference number 801-63787. Registered in England and Wales, Company Number 02080604.

All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without prior written permission from W1M Wealth Management Limited.

Copyright © 2025 W1M Wealth Management Limited.