Portfolio activity amidst Middle East tensions

Summary

- Tightening liquidity, rising inflation, slower growth are all likely

- Reduced equity weight across the multi-asset funds over the past three weeks

- Sold US Treasuries in the Multi-Asset Income Fund

- Reduced duration across all Multi-Asset Funds

Softening economic outlook

The hostilities in Iran and the Middle East will likely result in a tightening of global liquidity, a rise in inflation and a reduction in the growth rate. These three factors have led us to bring our outlook for the economy down a notch.

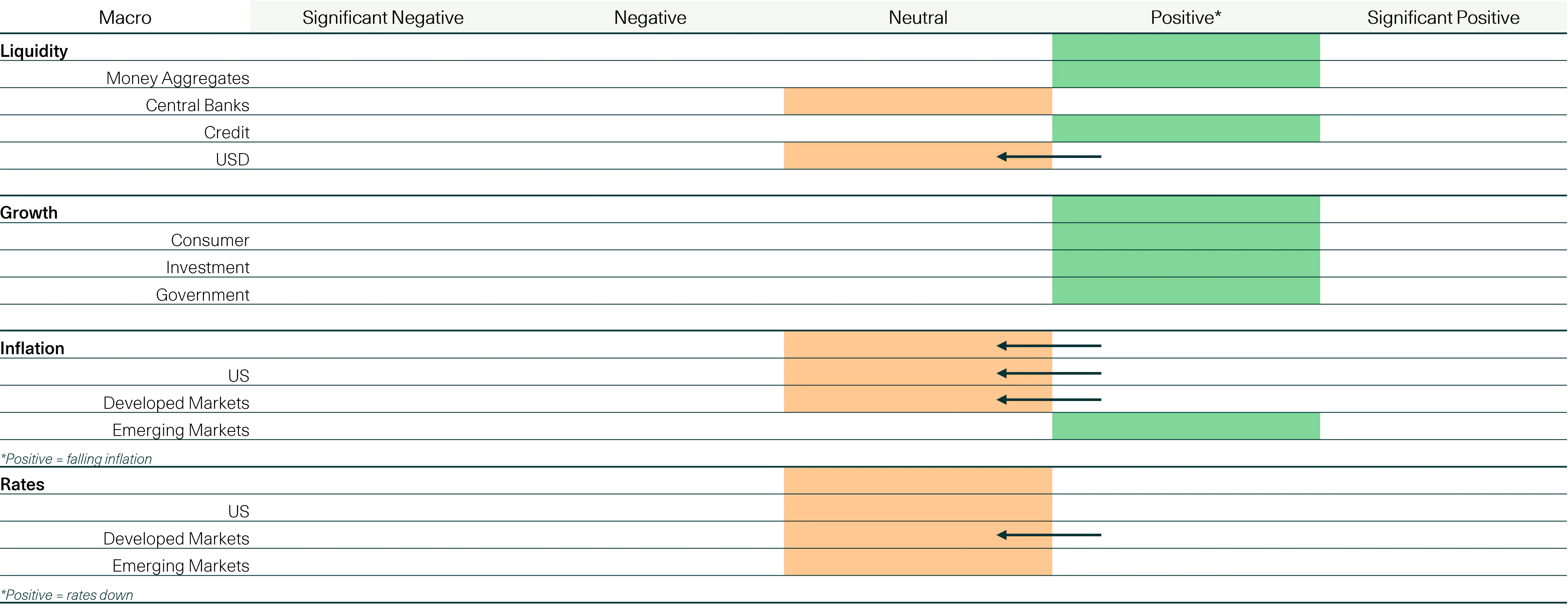

Changes to economic outlook

Source: W1M, 28.02.2026

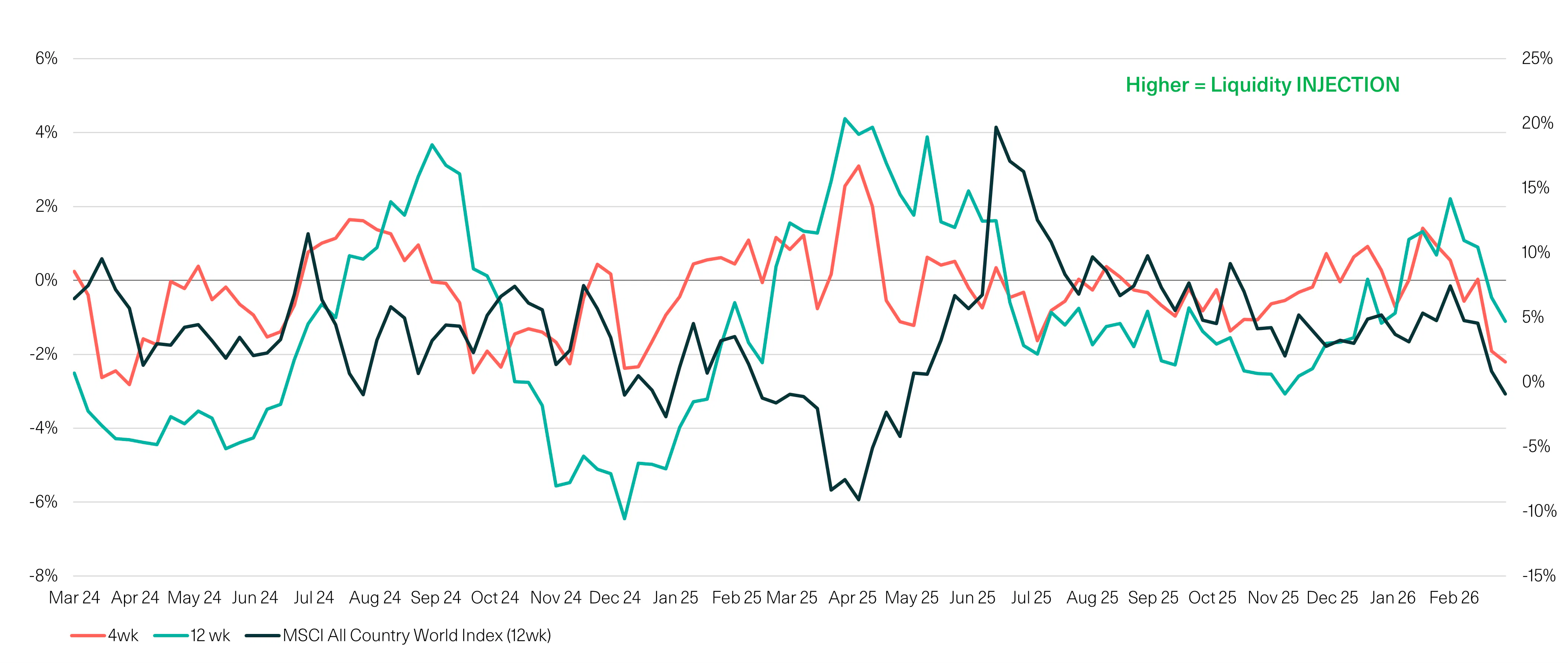

Reduced Liquidity Support: 4 & 12 week change in Central Bank Balance Sheets & 12 week change in Global Equities

Source: W1M, Bloomberg 19.03.2026

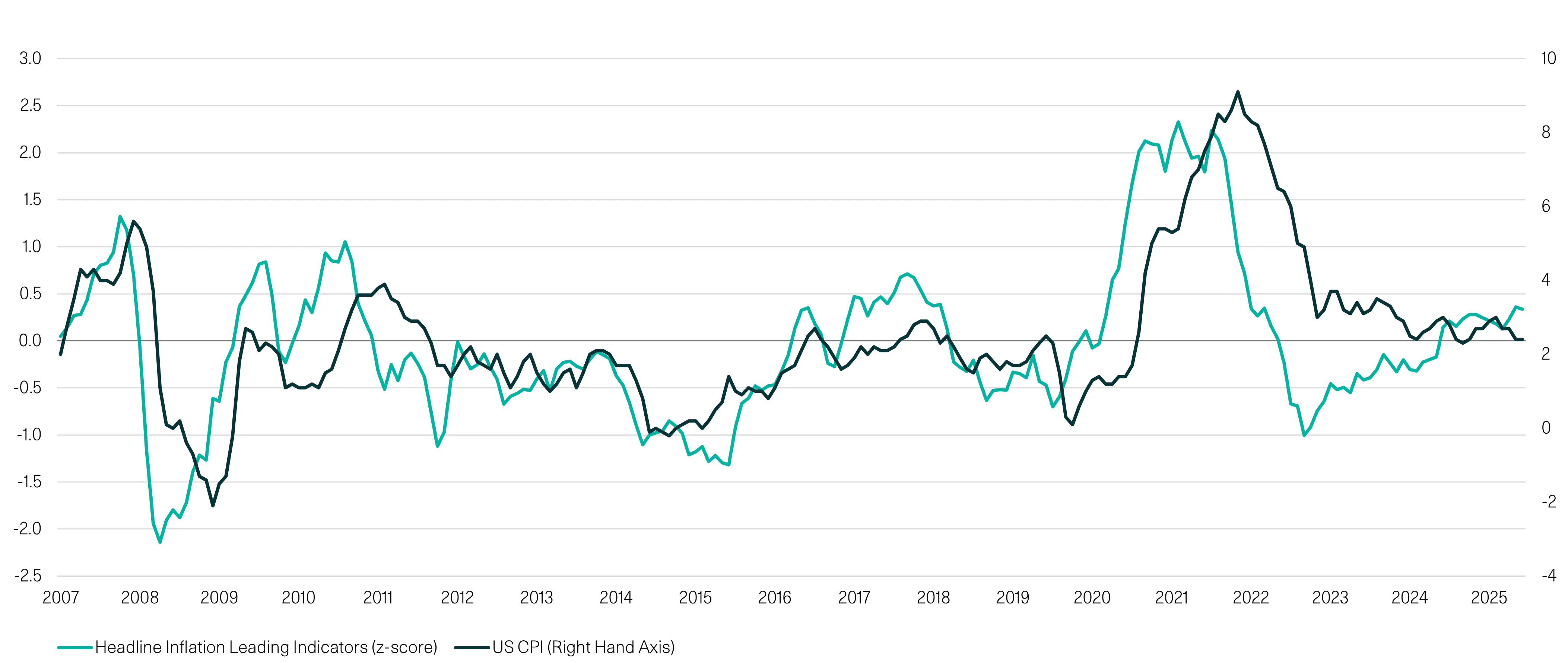

US CPI Leading Indicator & US CPI

Source: W1M, Bloomberg 19.03.2026

Market reaction

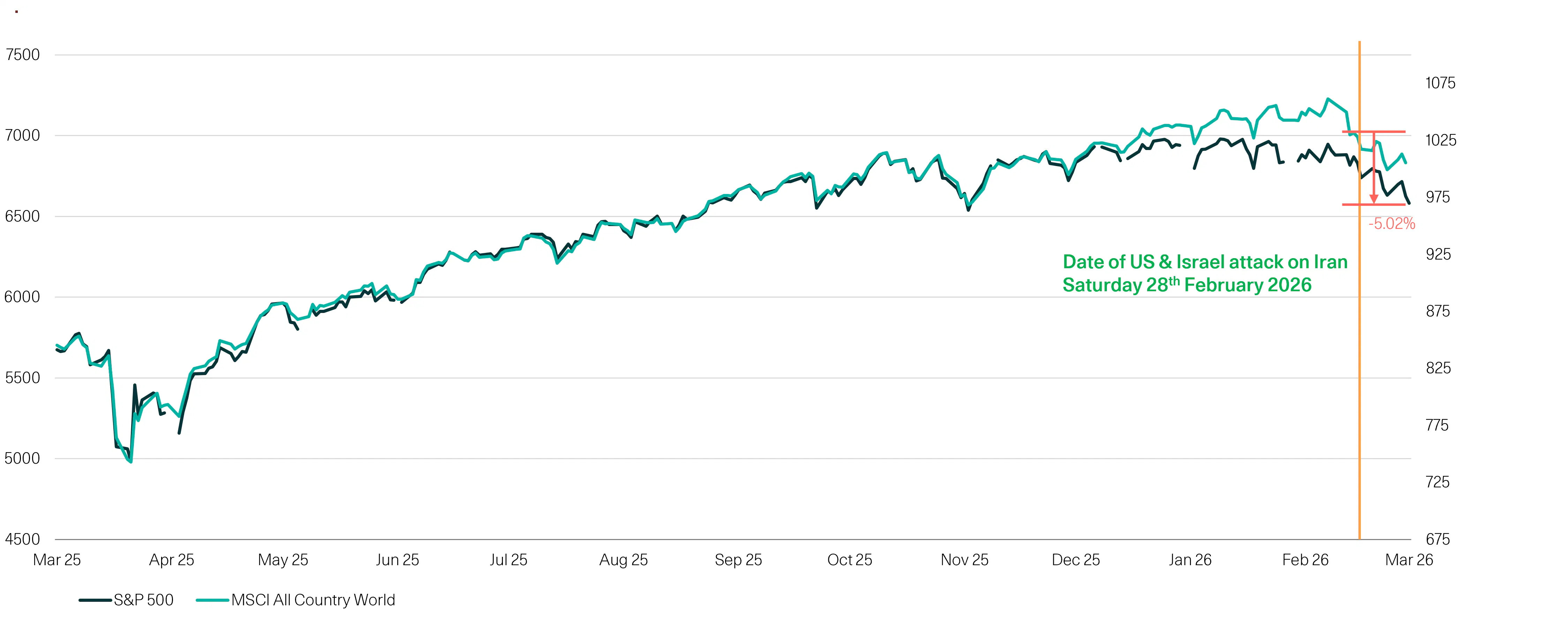

Until the latter half of this week, headline equity markets had not materially moved; indeed, the S&P 500 is still only off -5%, and the Global equity market just -6%. Sentiment has shifted weaker, but positioning has remained very full and flows into equity markets have been positive. Retail investors, conditioned to buy the dip in the post-Covid period, have been rewarded for doing so until now, and appear to have followed the same approach this time round.

US & Global Equity markets (1-year)

A weakening economic outlook with risk assets barely re-pricing a risk which itself increases exponentially as time passes has given us the opportunity to reduce risk in the Multi-Asset Funds.

Action taken

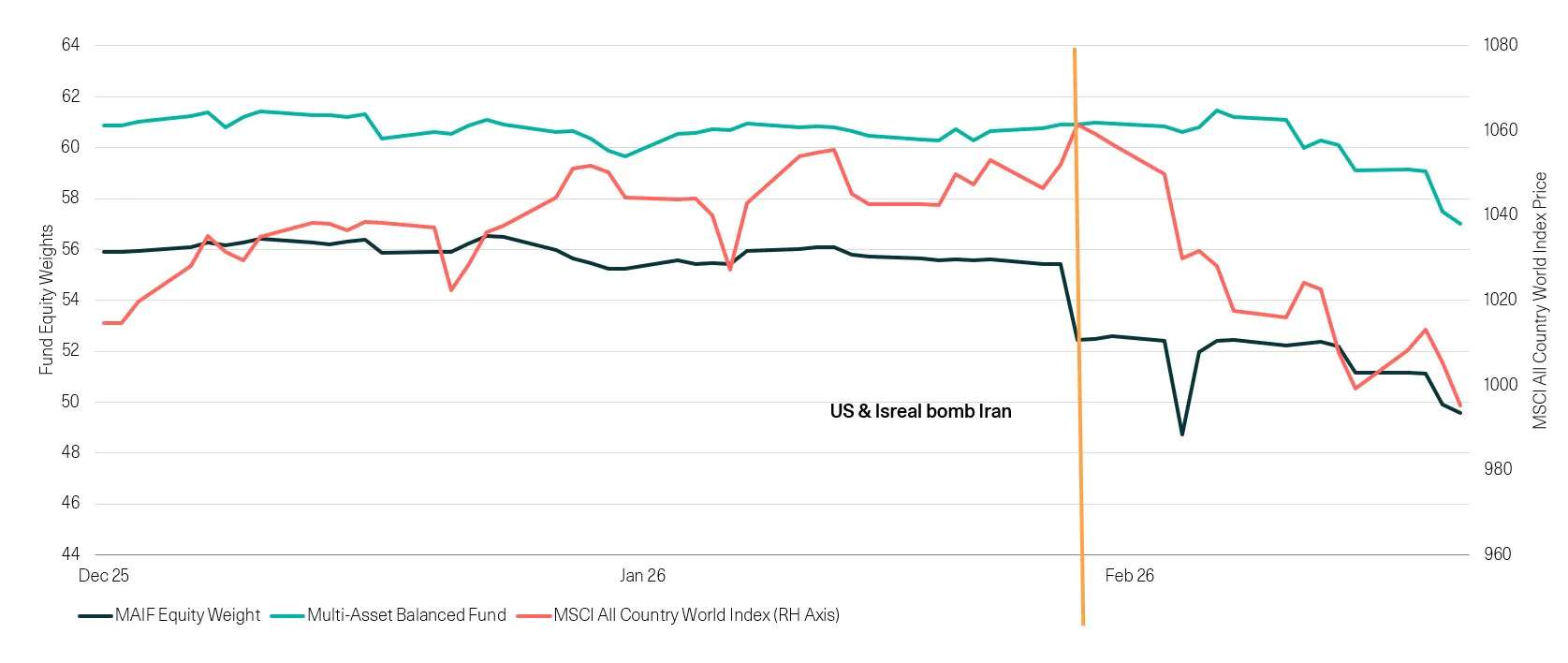

In the Multi-Asset Income Fund, we took 3% out of equity risk the day before the attack on Iran, not because we anticipated the war, but because we could see inflationary pressures building in the US while the market was pricing a very dovish outlook from the Federal Reserve. In the following weeks, we have reduced equities further, taking a full 5% out of equities. Similarly, in the Multi-Asset Fund range we have taken risk off the table, bringing the fund from slightly overweight risk at the beginning of the year to ~2.5% underweight equities across the piece as I write.

Multi-Asset Fund Equity Weights & MSCI All Country World Index

Source: Factset

These are tactical moves, consistent with our approach of “incrementalism”: incrementally building into or out of a position as the data confirms the thesis (or otherwise). The news flow on the Iranian situation continues to track negatively, raising the ‘bear case’ probability in our framework. To us, the asymmetry remains to the downside, principally because of the ripple effect a long duration closure of the Straight of Hormuz (or other extended supply shock) will have on the economy.

We think Donald Trump is more inclined to deal than the Iranian theocracy at this stage. And though a tipping point will be reached where the Iranian leadership loses the faith of its people, it appears President Trump has already lost the backing of his: increasingly visible fractions within the Republican party, approval rates of both the war and President Trump himself tracking negatively, and price rises already feeding through to the consumer. In a Mid-Term year, this is politically perilous.

It appears Trump and the US have lost control of this war (if they ever had it) and have little control over the price of oil (if this were ever likely). In such a situation, we would not be surprised to see an attempt at a Hail Mary from the Executive: a payment directly to US Households to cover some of the increase in consumer bills. This was mooted late last year, and the sums amount to $450bn or so – a figure to add to the existing government deficit. Far from a given, but a genuine possibility, and coupled with the rising inflationary pressures already in the system and the energy price spike yet to hit the numbers, a good reason to take our US Treasury exposure in the Multi-Asset Income Fund to zero earlier in the month. (While on government bonds, it is worth noting that we brought our duration down to 6 years (from 7.5) across the multi-asset funds ahead of the Iran conflict.)

We came into the year with a fully-valued equity market and a goldilocks backdrop. The backdrop has changed and risk assets are beginning to price this. We will continue to incrementally adapt our positioning according to the 6-month outlook. We will write a fuller and more analytical piece outlining our outlook in the weeks to come.

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may rise as well as fall, and investors may not get back the amount originally invested. Capital security is not guaranteed.

This material is provided for informational purposes only and does not constitute investment advice or a recommendation. It should not be considered an offer to buy or sell any financial instrument or security. Any investment should be made based on a full understanding of the relevant documentation, including a private placement memorandum or offering documents where applicable. W1M Wealth Management Limited is authorised and regulated by both by the Financial Conduct Authority of 12 Endeavour Square, London E20 1JN, with firm reference number 120776 and the U.S. Securities and Exchange Commission of 100 F Street, NE Washington, DC 20549, with firm reference number 801-63787. Registered in England and Wales, Company Number 02080604.

All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without prior written permission from W1M Wealth Management Limited.

Copyright © 2026 W1M Wealth Management Limited.