Navigating choppy markets: Be properly diversified, global, active and direct

We have been writing about bubbles and diversification for a while; now that markets, after a great run this year, are a little more jittery, it may good to remember that we diversify exactly because there is greater volatility every now and then and portfolios must be able to cope and deliver on medium and long term objectives. In addition to diversifying across equities, bonds and real assets, however, W1M also has “protection strategies” which aim to protect capital in times of market nervousness.

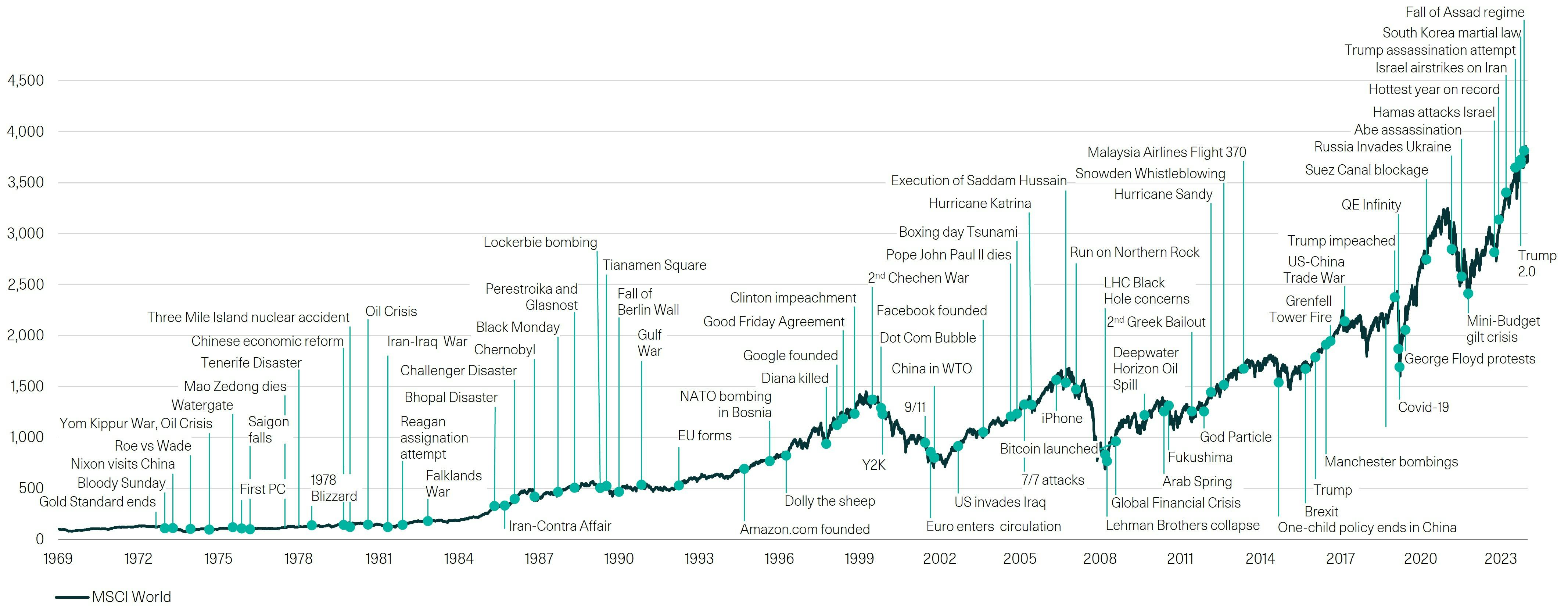

There's always a reason not to be invested...

"Climb the wall of worry"

Source: W1M, Bloomberg. As at 31.12.24.

Risk warning: Past performance is no guarantee of future results and the value and income from such investments and their strategies may fall as well as rise. You may not get back your initial investment. Capital security is not guaranteed.

There are always reasons not to invest and very few people have brilliant market timing which enables them to sell at the top and buy at the bottom. Unfortunately, “going to cash” can lead to buying back equities at higher prices. For the long term investor, the key question is not about trying to time the market but how to, diversify. At W1M we do not believe that buying every stock in the world is the best way to diversify in equities, especially when a handful of stocks now dominate even large indices like the S&P 500. An active equity portfolio with around fifty stocks could easily have less “AI” related tech exposure than an index fund bought perhaps in the expectation of it being more diversified given many more holdings. We believe that, in addition to diversification, adding “protection strategies” is useful in just the same way as most house owners take out some insurance to mitigate losses in extreme events. Not everyone has such strategies. Fixed income positioning can add to the defensiveness of a portfolio and holding real assets can give inflation resilience and good returns for the long term investor.

W1M

At W1M, we approach long-term investing by being global, active and direct; looking for the best ideas regardless of geography with dedicated investment analysts. Our philosophy is based on beating inflation because in the long run, what matters for the purchasing power of savers and investors in beating inflation. We have a long track record through economic cycles.

We have written about the risks of a few stocks being very large and dominating indices: The passive boom and why it could be the next big risk. Our equity portfolios do not own every stock in indices, nor do we hold all the “Magnificent Seven” stocks. We have discussed our equity investment approach in a world with some pockets of high valuation and markets not far from all time highs.

Magnificent Seven at a record 32% of S&P500 market capitalisation

Magnificent Seven Index as % of Market Capitalisation of S&P500 Index 2016 - current, weekly

Source: Bloomberg, W1M. As at 17.10.25

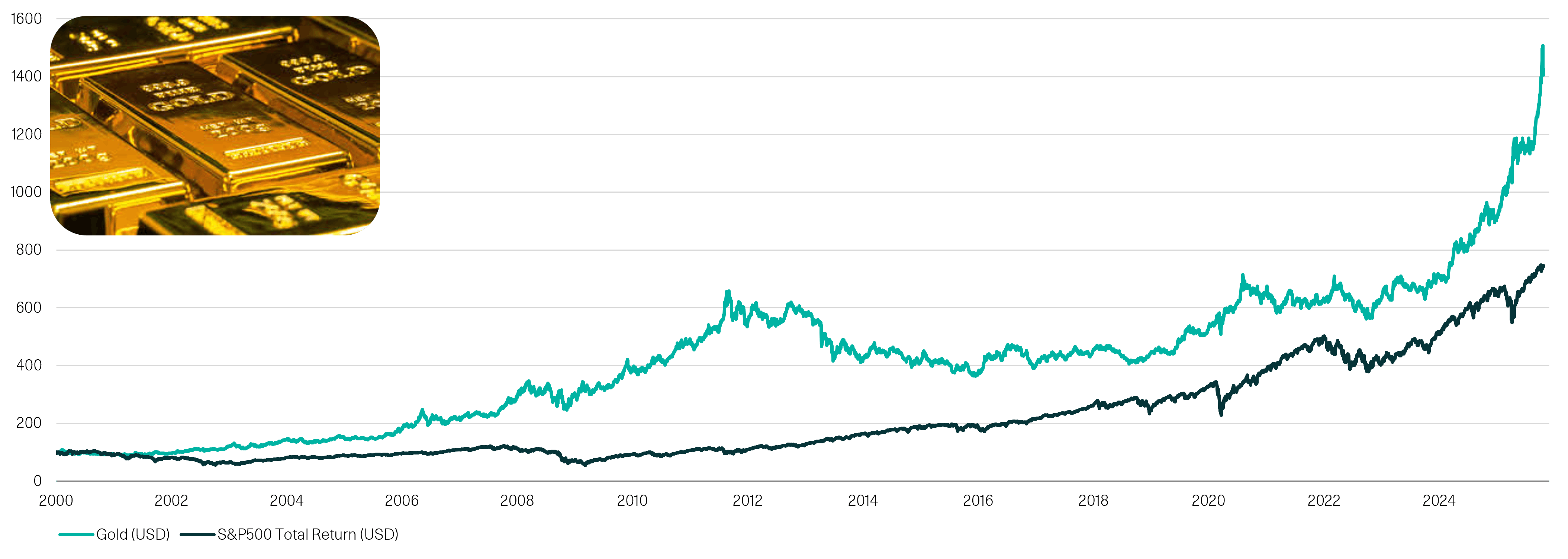

While we are able to find very interesting global investment ideas even in current equity markets, including real assets in the portfolio gives inflation resilience and improves the risk adjusted prospects of portfolios. Gold has done well and could have further to go, given central bank for the metal is now strong, but real assets are not just about gold and we have written about uranium and energy related holdings recently.

Real Assets and Absolute Return strategies can provide uncorrelated protection against equity risks

Gold has recovered strongly in the 21st Century

Source: Bloomberg, W1M. Data as of 24.10.25

Risk warning: The information above is for example purposes only and should not be considered a solicitation to buy or an offer to sell a security. It is based on our current view of markets and is subject to change. Past performance is no guarantee of future results and the value and income from such investments and their strategies may fall as well as rise. You may not get back your initial investment. Capital security is not guaranteed.

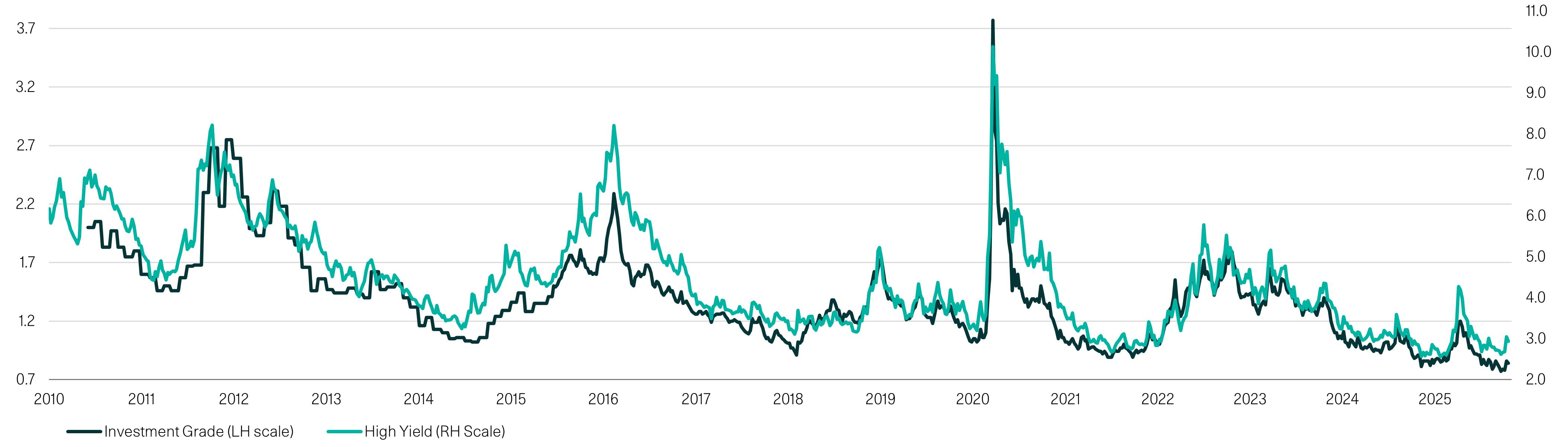

In fixed income, we have a cautious stance, favouring gilts over credit in the belief that UK inflation can fall sharply in the next year and gilts can outperform. We are not not necessarily negative on credit but it is hard to argue that it is “cheap” but we see potentially better returns in gilts over the next year. If markets get more volatile, particularly if concerns regarding growth increase and inflation reduces as a worry, this positioning could act as something of a buffer.

US corporate bond spreads (%)

Source: Markit, Bloomberg W1M. As at 17.10.25

Not everyone has a protection strategy. We have written before on how W1M multi asset portfolios incorporate investments which aim to mitigate losses in times of market stress. You can think of it as being similar to buying home insurance. Most people tend to spend a meaningful amount on house buildings and contents insurance in the hope of not having to use it. We pay a premium so that if the house burns down, we get financial help to rebuild. For similar reasons, W1M does not just rely on diversification but also uses proprietary Protection Strategies. When markets are going up, there is a small cost for having derivative based positions which will pay out in the event of significant market stress, when such events occur, it is very helpful to have some “insurance”. Being active, enables investors to do more than just diversify but to be proactive about capital protection.

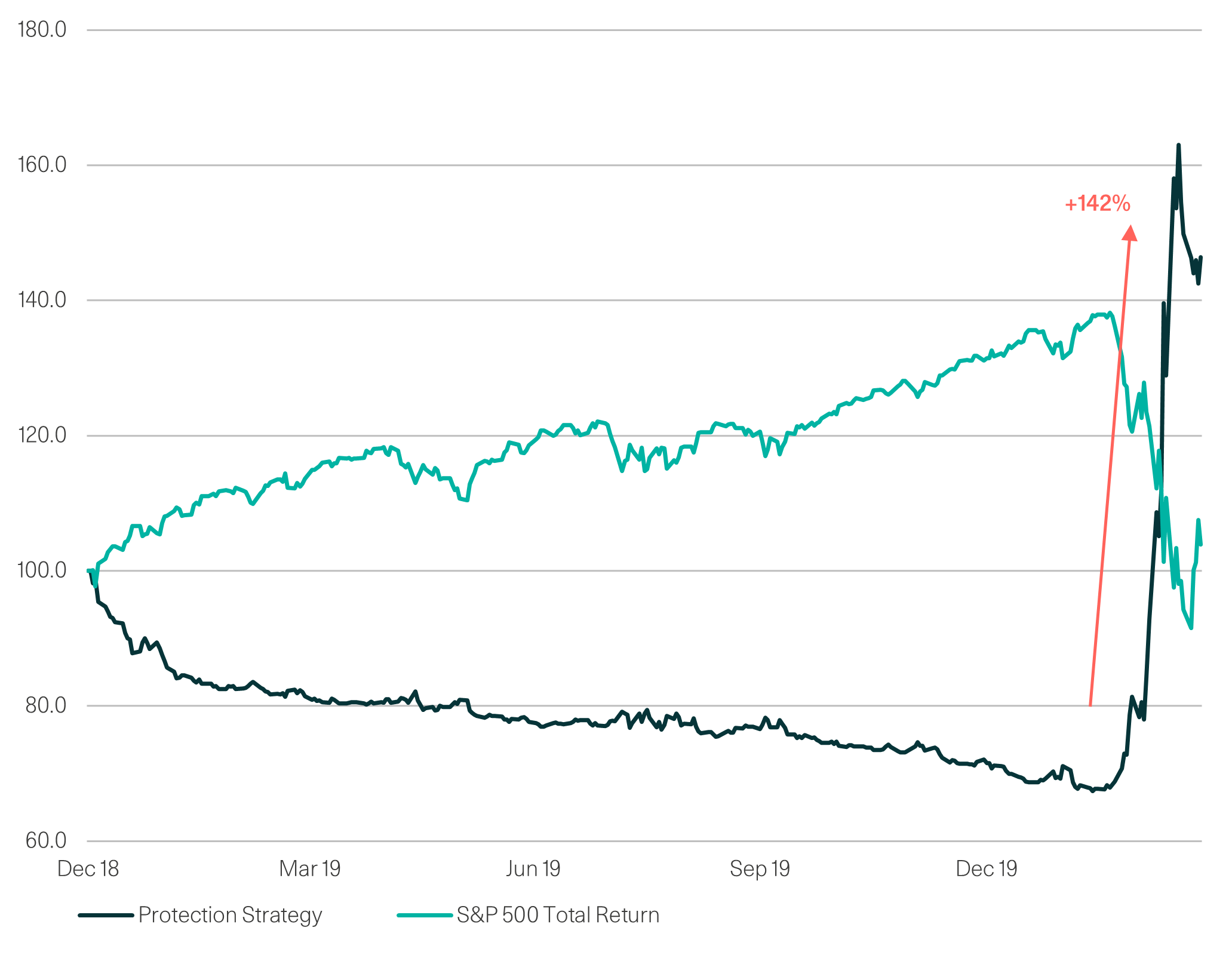

How Did it Perform (Vs. Design) During Covid-19 Crisis?

Actual PS performance vs S&P 500 (TR)

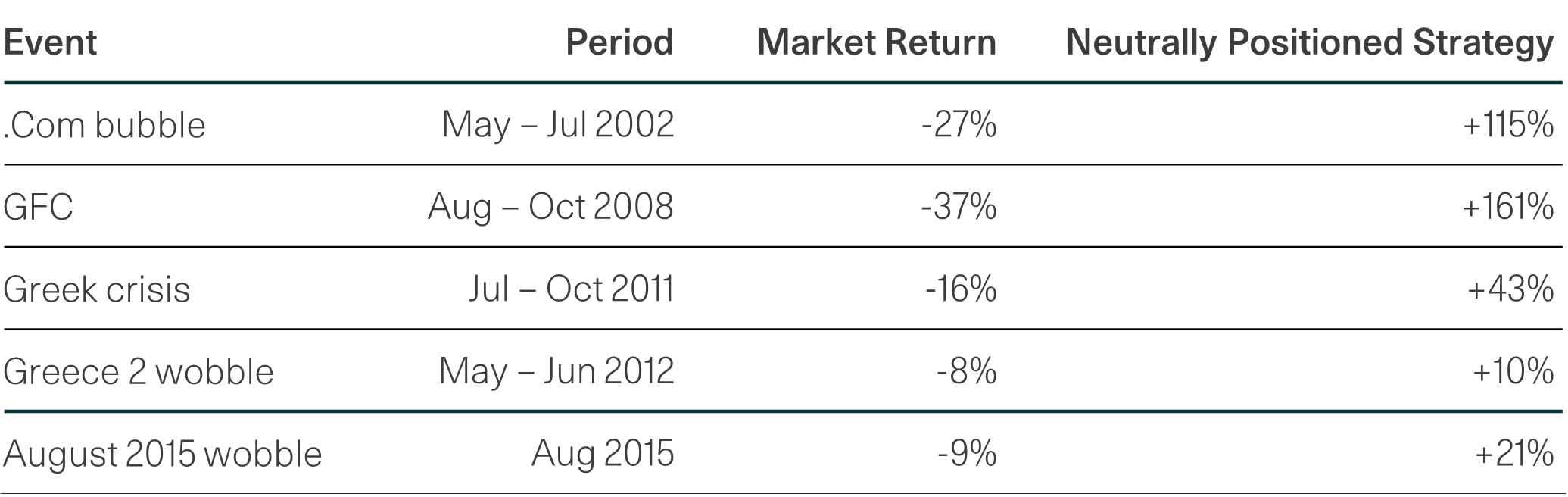

Back-tested returns in previous crises

*Inception: 19th April 2016 Data to from 31.12.19 to 31.03.20

Source: Goldman Sachs, Bloomberg, W1M.

Figures are calculated on a total return basis, net of fees.

Risk Warning: Past performance and simulated past performance is no guarantee of future results and the value of such investments and their strategies may fall as well as rise.

You may not get back your initial investment. Capital security is not guaranteed.

In summary, we do not believe we or anyone else will be able to time the markets perfectly. That is not a controversial belief. What we do know if that through economic cycles and crises, being properly diversified, global, active and direct.

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may rise as well as fall, and investors may not get back the amount originally invested. Capital security is not guaranteed.

This material is provided for informational purposes only and does not constitute investment advice or a recommendation. It should not be considered an offer to buy or sell any financial instrument or security. Any investment should be made based on a full understanding of the relevant documentation, including a private placement memorandum or offering documents where applicable. W1M Wealth Management Limited is authorised and regulated by both by the Financial Conduct Authority of 12 Endeavour Square, London E20 1JN, with firm reference number 120776 and the U.S. Securities and Exchange Commission of 100 F Street, NE Washington, DC 20549, with firm reference number 801-63787. Registered in England and Wales, Company Number 02080604.

All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without prior written permission from W1M Wealth Management Limited.

Copyright © 2025 W1M Wealth Management Limited.