Market Perspectives April 2026

View the full PDF document including total return indices, click here.

The Outlook for Interest Rates

Gilts suffered a reversal on the outbreak of war.

Gilts performed well in January and February as weak economic growth and benign inflation figures encouraged investors to believe that the Bank of England would cut interest rates at least twice this year. The day before the Iran war broke out, the 10-year gilt yield troughed at 4.25% – its lowest level for over a year. However, all that changed as soon as the oil price rose, whereupon the inflation outlook changed overnight: yields soon reached 5% as the market started to discount two base rate hikes instead of two cuts.

It is not only oil and gas which face supply constraints.

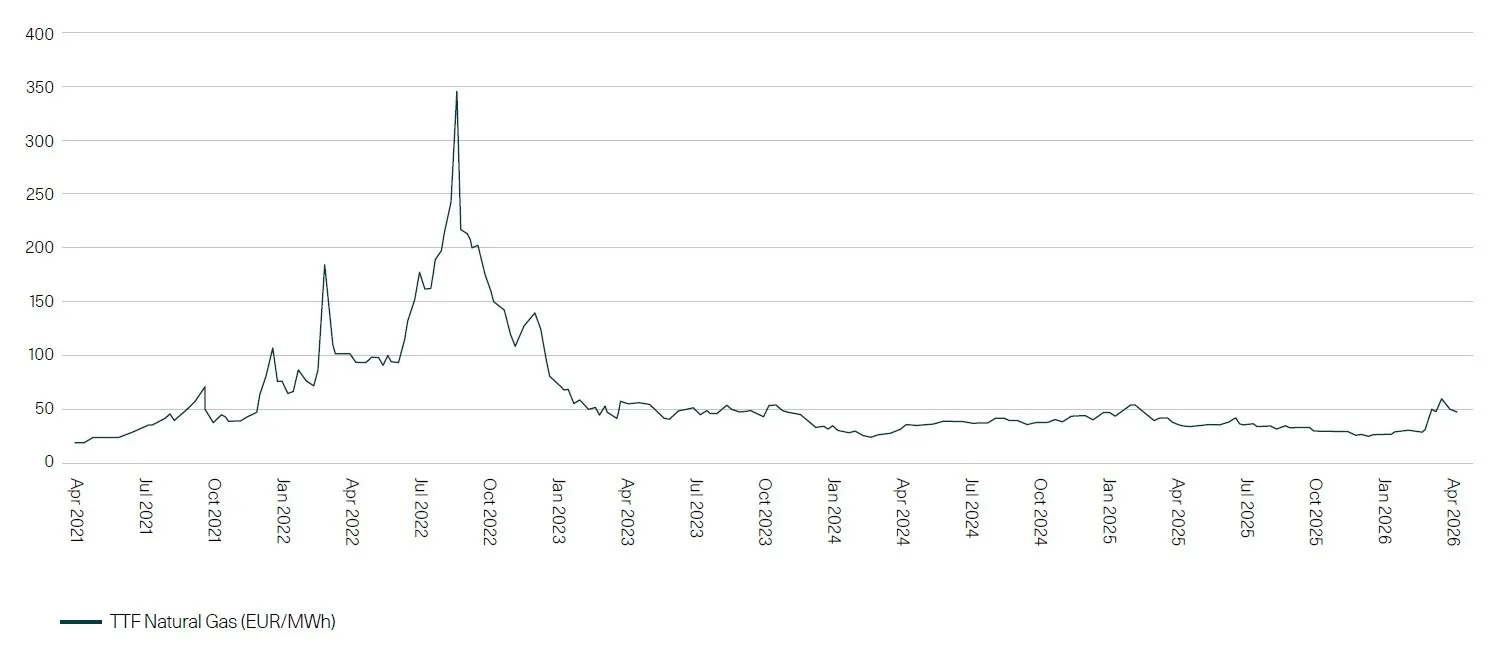

There is no doubt that the rise in oil and gas prices that we have already seen will lead to an increase in inflation. Moreover, the effective closure of the Strait of Hormuz has had an impact on the supply of numerous commodities other than hydrocarbons: for example, the Persian Gulf is a major exporter of fertilizer, a shortage of which during the growing season will have a knock-on effect on food prices around the world – bringing further challenge to an agriculture sector which is already nervous about the availability of diesel. Also, the aluminium price has reached a four-year high after smelters in Abu Dhabi and Bahrain were hit by Iranian missiles. The supply of helium is a another concern as it is an important by product of natural gas processing – so Qatar accounts for nearly a third of global helium production; the inert gas is critical for semiconductor manufacturing and the operation of MRI scanners.

The inflationary impact is likely to be widespread.

Although, so far, the oil price has not risen as much as it did after the outbreak of war in Ukraine, and the European gas price remains far below its 2022 peak, a prolonged closure of the Strait of Hormuz would likely be more widely felt because a higher percentage of global commodity supply is affected. Qatar accounts for 20% of global LNG production and, whereas Russia’s oil and gas was largely redirected away from Western Europe to other markets, in the Middle East oil and gas production has been physically disabled, and that which is being produced cannot easily find other routes to market.

However, it may not be as acute in the UK as it was in 2022.

The inflation impact in the UK may not be as bad as it was in 2022, when CPI peaked at over 11%. Four years ago there was huge pent-up demand in the economy from Covid, interest rates were still very low and quantitative easing (‘money printing’) had only recently come to an end. In contrast, this time the economy is moribund, there is a lot of slack in the labour market and interest rates – as far as bond yields’ impact on the mortgage market is concerned – are already restrictive. It may well be, therefore, that the Bank of England does not need to raise the Base Rate as much as is currently discounted.

There are pockets of value in the bond markets.

The situation in the US is slightly different: there, the first order effects on inflation of the current crisis are likely to be lower by virtue of the United States’ self-sufficiency in hydrocarbons: current estimates are that the immediate effect of higher energy costs will add about 1% to US CPI. However, the second order effects may be more difficult to curtail as the economy is doing well and the labour market is strong. Either way, it’s difficult to be bullish on bonds whilst the outlook for inflation and interest rates is so uncertain. However (recognising that gilt yields are moving significantly on a daily basis), we can say that, as at the end of March, the short end of the curve is low risk and looks attractive because it discounts two rate rises that we do not think will be forthcoming; and at the longer end, a nine year ultra-low coupon gilt now yields 8.2% gross equivalent to a 45% taxpayer; finally, index-linked securities (including TIPS in the US) offer both decent real yields and inflation protection.

European Gas Price

Source: W1M / Factset.

The Outlook for Equities

Equities have fallen in sympathy with bond yields.

Until the outbreak of war, equities were doing well as the US economy was chugging along, bond yields were falling and corporate results were coming in line with, or even slightly ahead of expectations. On initial hostilities, markets were not unduly affected because it looked like there was every chance this would be a short affair like January’s operation in Venezuela or the bombing of Iran last June. However, as it become clear that regime change or unconditional surrender by Iran was not going to materialise quickly (if at all), world equities fell nearly 10% over the next four weeks. The effect of rising bond yields on valuations probably accounts for most of this decline because, as yet, aggregate earnings expectations have not been downgraded.

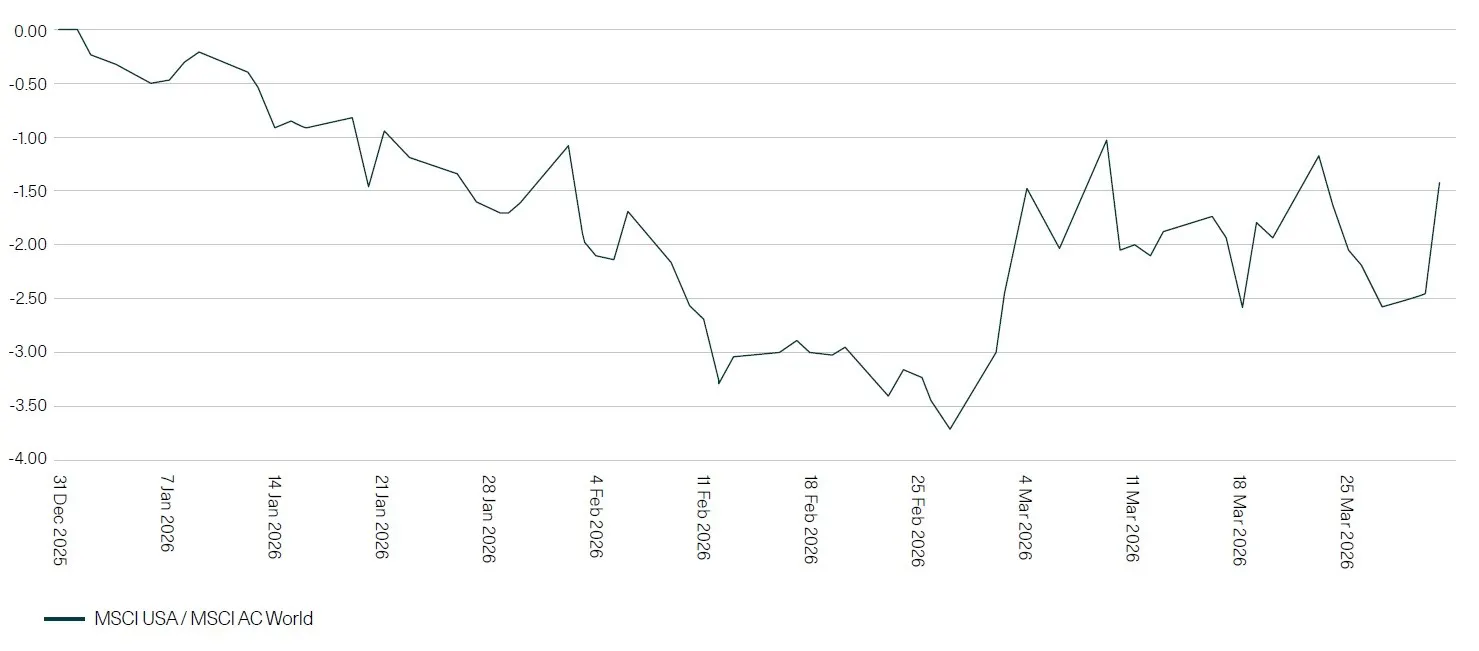

Since the outbreak of war, the US has outperformed.

The most notable falls have been seen in those areas which did well in the run-up to the war, and now faced sudden profit-taking on the tightening of liquidity – precious metals being a particular case in point. Geographically, Asia Pacific, Japan and Emerging Markets have been hit harder than the US because they are more exposed to the supply of Middle Eastern oil and gas; also, they were the strongest performing regions in the first two months of the year. The US stock market benefits from some sectoral advantages given its large technology component (although that is tempered by the fact that, apart from the giants that dominate the index, many US tech companies are on very high multiples, and therefore more vulnerable to rising bond yields). The wide range of outcomes together with the extreme unpredictability of President Trump’s social media posts (which are often directly contradicted only a day or two later) mean that there has been considerable volatility in asset prices: there have been some big intra-day turnrounds in equity sentiment and long bond yields which are hidden from daily closing prices. In such an environment it is important not to trade on news flow as the risk of whipsaw is high.

We have reviewed all our exposures, and maintain appropriate levels of diversification.

We have not been sitting on our hands during this period, as we have used significant price movements to edge more money into defensives such as Air Liquide, and reduce exposure to cyclicals which have done well like SMFG and CATL. We have also classified each one of our recommended equity holdings by their sensitivity to the current situation. Most exposed to oil and gas prices are companies like Smurfit Westrock and Grab Holdings (with their high energy use); least sensitive are the likes of Tencent, Thermo Fisher and AstraZeneca. Outright beneficiaries include Shell (as a producer of hydrocarbons), CME (which thrives on market volatility) and IHI (exposure to the defence industry). The uncertain length and unpredictable outcome of this war means that it would be folly not to have a balance of representation in any portfolio – but at the same time we must make sure that each individual holding stacks up not solely because it represents a play on one macro input or another (falling oil prices / rising interest rates etc.), but because it merits inclusion as a core long term compounder or a structural improver. That way, we have a much better chance of ensuring that our portfolios, for all the buffeting that they will suffer as the news changes, have a high chance of outperforming in the long run regardless of the short run noise.

Earnings forecasts are the key to future returns.

Equity valuations have come down but the key to returns from here to the end of the year is likely to be what happens to earnings forecasts. If recession can be avoided and companies are able to adapt to what is being thrown at them (as they did surprisingly well last year in the face of broad-based and punitive tariffs), then we should be able to make progress once again. In the meantime, we stay neutrally weighted towards equities, underweight fixed interest and overweight alternatives – increasingly, in the current climate, to ‘absolute return’ assets which we believe can hold their value in a variety of conditions, and negatively correlated solutions like our Protection Strategy.

US Stock Market relative to World Stock Markets

Source: W1M / Factset.

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may rise as

well as fall, and investors may not get back the amount originally invested. Capital security is not guaranteed.

This material is provided for informational purposes only and does not constitute investment advice or a recommendation. It should not be considered an offer to buy or sell any financial instrument or security. Any investment should be made based on a full understanding of the relevant documentation, including a private placement memorandum or offering documents where applicable. W1M Wealth Management Limited is authorised and regulated by both by the Financial Conduct Authority of 12 Endeavour Square, London E20 1JN, with firm reference number 120776 and the U.S. Securities and Exchange Commission of 100 F Street, NE Washington, DC 20549, with firm reference number 801-63787. Registered in England and Wales, Company Number 02080604.

All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without prior written permission from W1M Wealth Management Limited.

Copyright © 2026 W1M Wealth Management Limited.

Market Perspectives April 2026