Inflation resilience needed

With a broadening Middle Eastern conflict (see Middle East first take | W1M), markets naturally think about inflation risks. Portfolios need to be properly diversified and international regarding mitigating volatility and delivering inflation resilience. Inflation had a post-pandemic resurgence after the invasion of Ukraine in 2022 impacted energy and food prices globally. It had been moderating and bond markets have been expecting one or two US and UK interest rate cuts this year, however, the latest geopolitical shock to markets is potentially inflationary.

Inflation risks are up again:

- Oil prices have been falling and supportive of growth recently, but have now jumped and, at around $73 (West Texas intermediate), around 26% year-to-date and $81 (Brent Crude) up around 32% year-to-date;

- Natural gas prices have spiked with UK prices up more than 40% compared to a month ago (which can impact UK heating costs, in time);

- Freight rates: Uncertainty persists as Iran announced the closing of the Strait of Hormuz through which around 20% of global oil and gas is shipped.

Inflation is a risk for both bonds and equities; this points to the need for greater diversification.

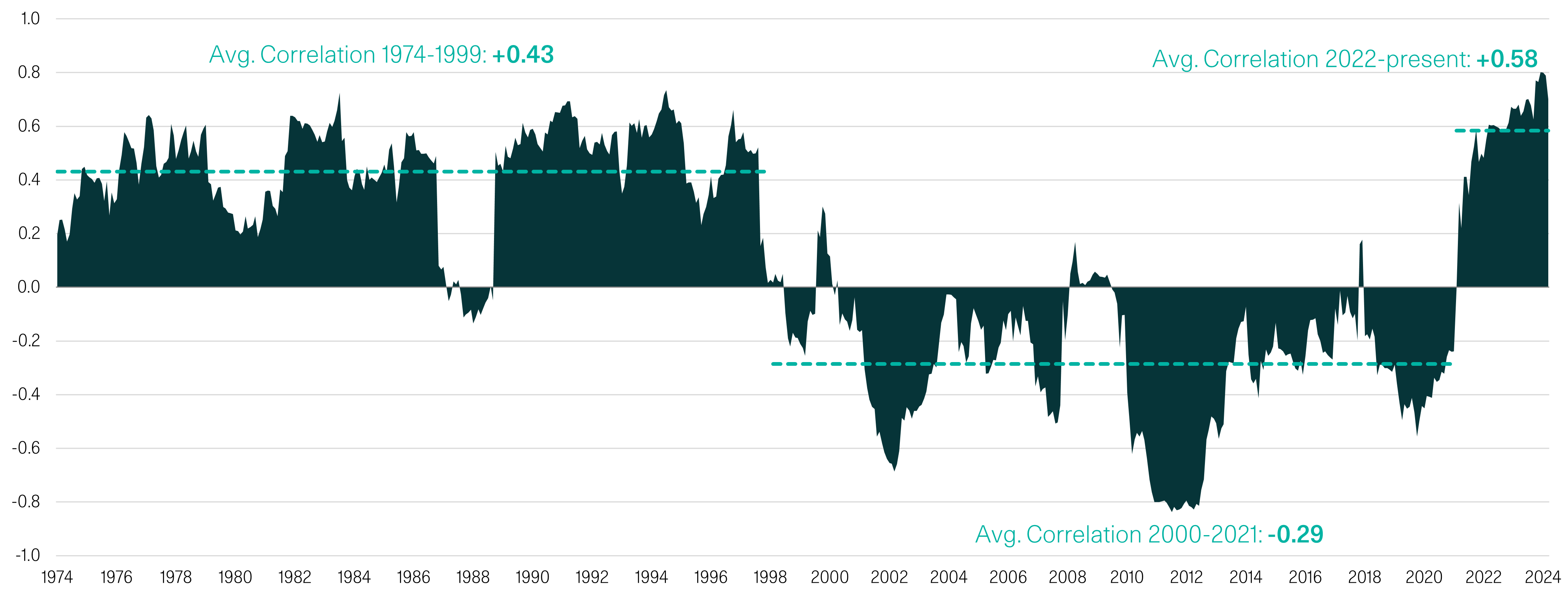

Bonds can fall with equities if inflation and interest rates rise

A traditional 60/40 portfolio is not offering the 'natural' diversification it once did

Source: Bloomberg, W1M. Data as at 30th June 2025.

Be properly diversified

Diversification is always important. The whole point of being diversified is that when some asset classes are negatively impacted, say by greater inflation risk putting upward pressure on interest rates, other assets can be uncorrelated and go up. If bonds (fixed income) are negatively impacted by inflation eroding the value of annual payments and fall in price when rates go up, it is a benefit to portfolios if asset classes, such as commodities / real assets are included to give resilience. If equities are negatively impacted by interest rates facing greater inflation risks because growth becomes more challenged, it is important for portfolios to be proactive in mitigating volatility.

Alternatives can be a hedge against geopolitical and inflation risk

Real Assets diversify portfolios and give inflation resilience

If energy and other production costs rise, miners of gold, for example, have to seek higher prices or make a loss. This is the basic mechanism which should give real assets inflation resilience if producers are rational. Supply should reduce ultimately if production is loss making. In addition to this inflation resilience quality, investors also value diversification away from fiat currency debasement. Our Real Assets Fund has significant exposure to gold and gold miners and this benefits our multi asset solutions in times of geopolitical risk.

Gold has been rising, but so has the stock market…is it expensive?

Gold price per troy ounce relative to S&P500 Index price - 1971 – current monthly

Source: Bloomberg, W1M. As at 31.01.26

Gold has had a strong run but the chart above shows that it is not necessarily “expensive” relative to equities.

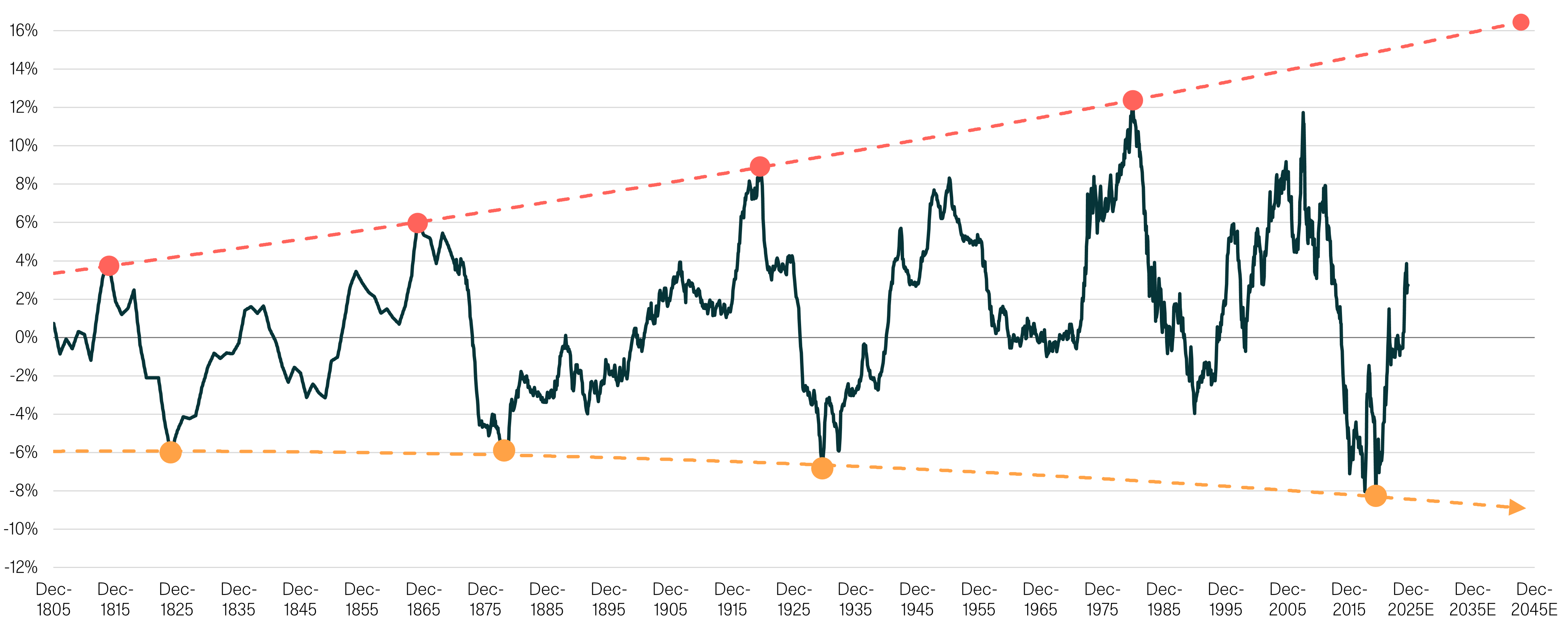

Commodities in a new supercycle?

Our Real Assets exposure is not just about holding gold, of course. Given huge potential demand for, inter alia, copper (electrification of transport and manufacturing) and uranium (nuclear power), we see a broader commodity cycle which is not necessarily peaking. Global growth being resilient, despite geopolitical shocks, matters, of course, for commodity demand in the shorter run; but, there are longer term, structural demand-drivers for commodities.

Long term commodity cycle showing signs of recovery

U.S. Commodity Price Index (Data 1795 to Present) with Major Inflation Peaks (Red Dots) & Major Inflation Troughs (Orange Dots)

Source: Stifel, W1M, Bloomberg. As at 31.12.25.

Be properly diversified in Equities

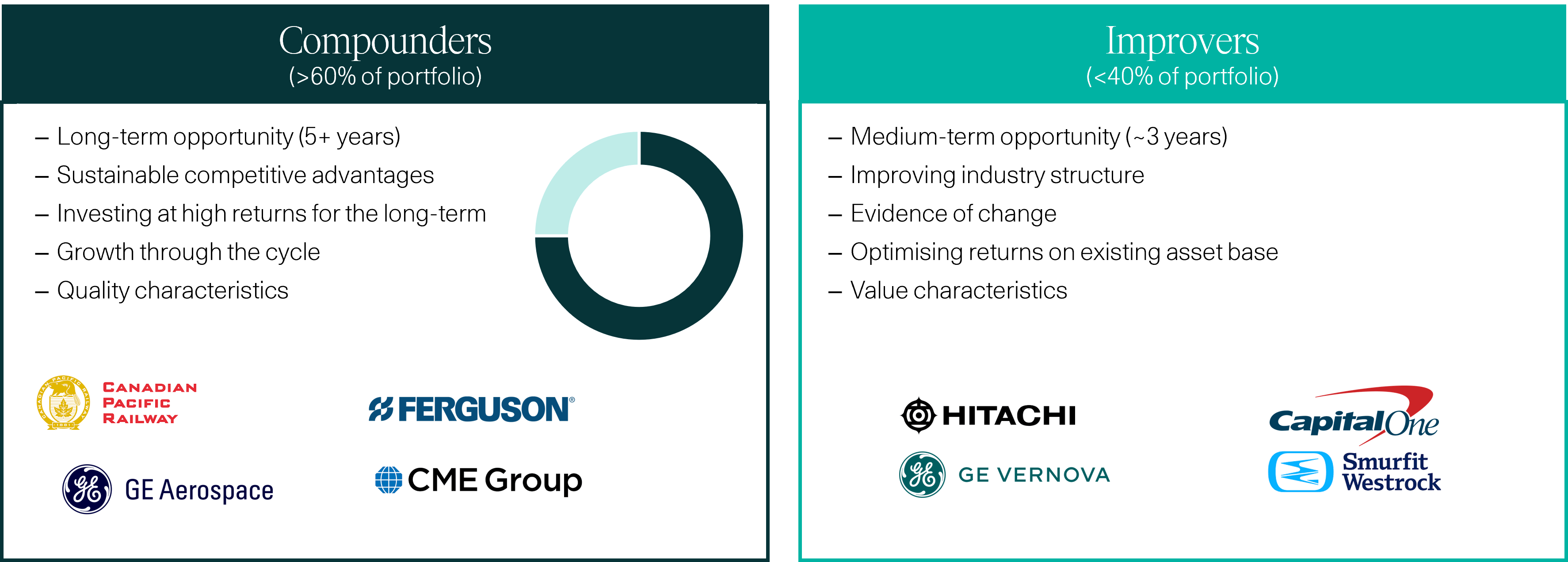

Active Equity stock selection

We invest in companies where the market underappreciates the quality of the business. This can either be the long-term sustainability of high returns or the improving fundamentals. We call these “Compounders” and “Improvers”.

Source: W1M, Google Images. As at 31.12.2025

Risk warning: This allocation should be used as a guide only. Differing market conditions may mean the above weightings will decrease or increase tactically. The investments listed are for example purposes and should not be considered as advice or a solicitation to buy or an offer to sell a security.

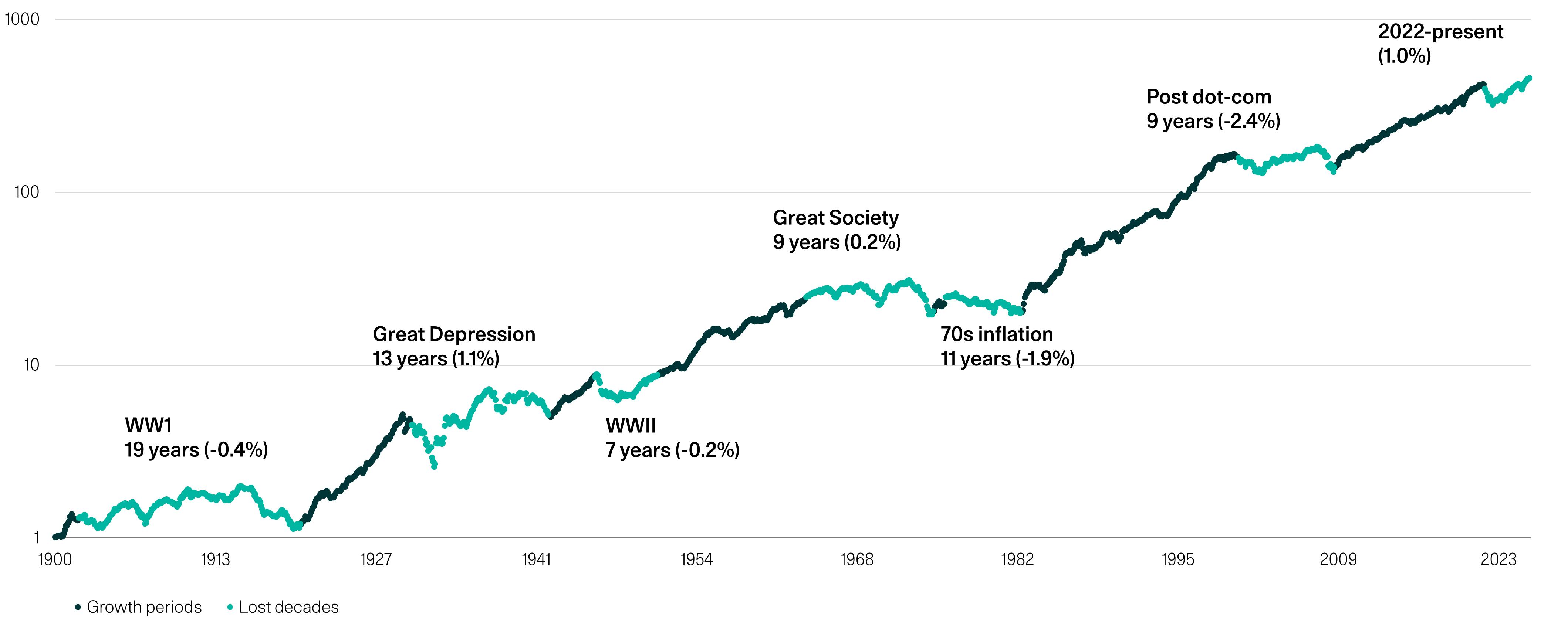

Our Active equity portfolios do not hold every stock in the index. We can choose not to hold airlines or not to hold all the biggest tech companies regardless of valuations. Passive funds can be useful but do not always outperform. In times of inflation risk increasing, holding passive investments can require a lot of patience as they can have lost decades.

Passive 60/40 portfolios have endured 6 "lost decades" since 1900; could we be entering no. 7?

Source: BofA, Bloomberg. As at 31.12.25. Note: 60/40 = 60% S&P 500 real total return and 40% US 10-year bond real total return

Risk warning: Past performance is no guarantee of future results.

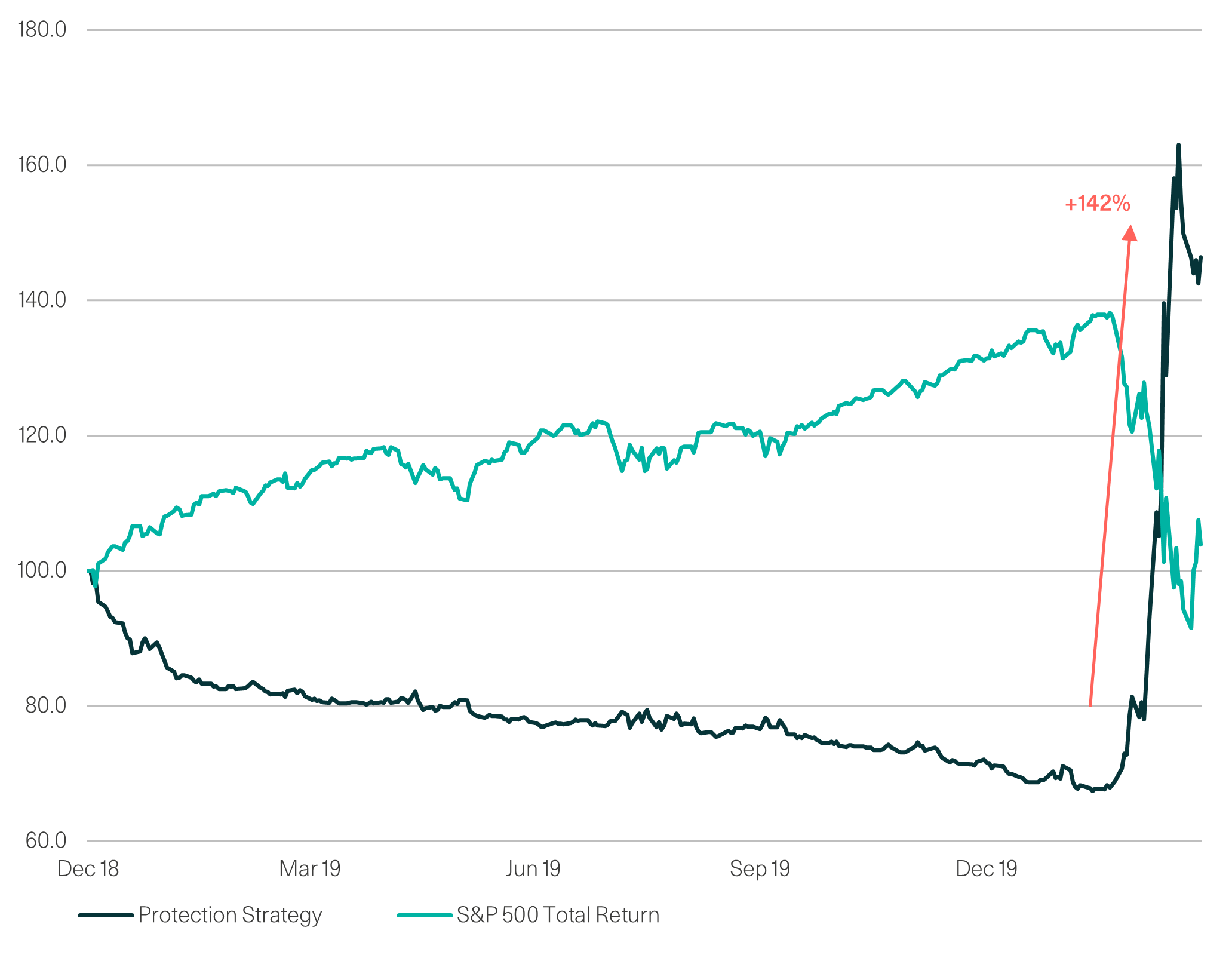

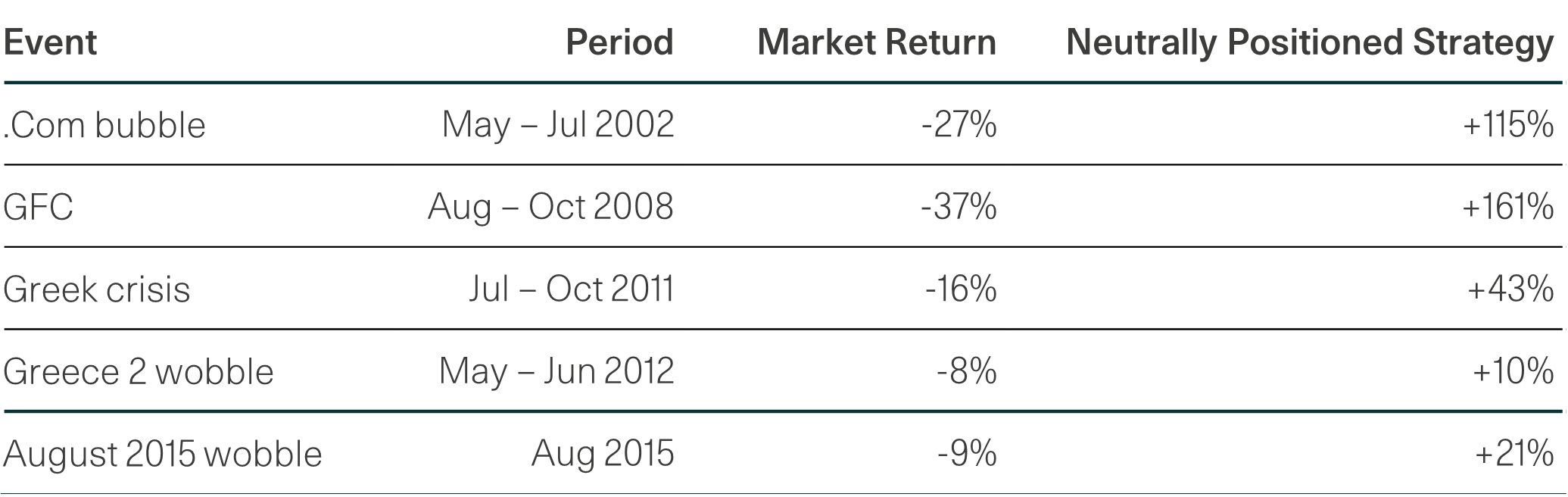

Protection Strategies

If you expect volatility, do you have a Protection Strategy? How did it perform during Covid-19 Crisis?

Actual PS performance vs S&P 500 (TR)

Back-tested returns in previous crises

In addition to being properly diversified, we design and deploy protection strategies to mitigate risks across our multi asset solutions.

*Inception: 19th April 2016 Data to from 31.12.19 to 31.03.20

Source: Goldman Sachs, Bloomberg, W1M.

Figures are calculated on a total return basis, net of fees.

Risk Warning: Past performance and simulated past performance is no guarantee of future results and the value of such investments and their strategies may fall as well as rise. You may not get back your initial investment. Capital security is not guaranteed.

Summary

There’s always a reason not to be invested…

“Climbing the wall of worry”

We do not invest based on market sentiment driven by short-term news. Geopolitical events tend to matter only if they damage the growth or inflation outlook. There is always a reason not to invest but, in the long run, being invested has paid off. However, we believe it is right to be properly diversified, to incorporate asset classes which give inflation resilience and to actively protect portfolios to mitigate potential risks.

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may rise as well as fall, and investors may not get back the amount originally invested. Capital security is not guaranteed.

This material is provided for informational purposes only and does not constitute investment advice or a recommendation. It should not be considered an offer to buy or sell any financial instrument or security. Any investment should be made based on a full understanding of the relevant documentation, including a private placement memorandum or offering documents where applicable.