Consumer Duty and the need for genuine diversification on your MPS panel

The Consumer Duty places a clear focus on transparency, accountability and, above all, the delivery of fair value to clients. At the same time, the rapid expansion and crowded nature of the Managed Portfolio Service market has created a new challenge for financial advisers and paraplanners: how to achieve meaningful differentiation.

The market is widely viewed as increasingly homogenous. Similar asset allocations, overlapping holdings and comparable investment approaches make it difficult for portfolios to stand out and for advisers to construct a panel that delivers genuine diversification.

A market drifting toward homogeneity

As cost pressure intensifies, many active managers have reduced expenses by shifting equity exposure into passive vehicles, resulting in similar holdings and asset allocations across portfolio providers. This convergence means that even blending multiple providers may add little incremental diversification if the underlying exposures are effectively the same.

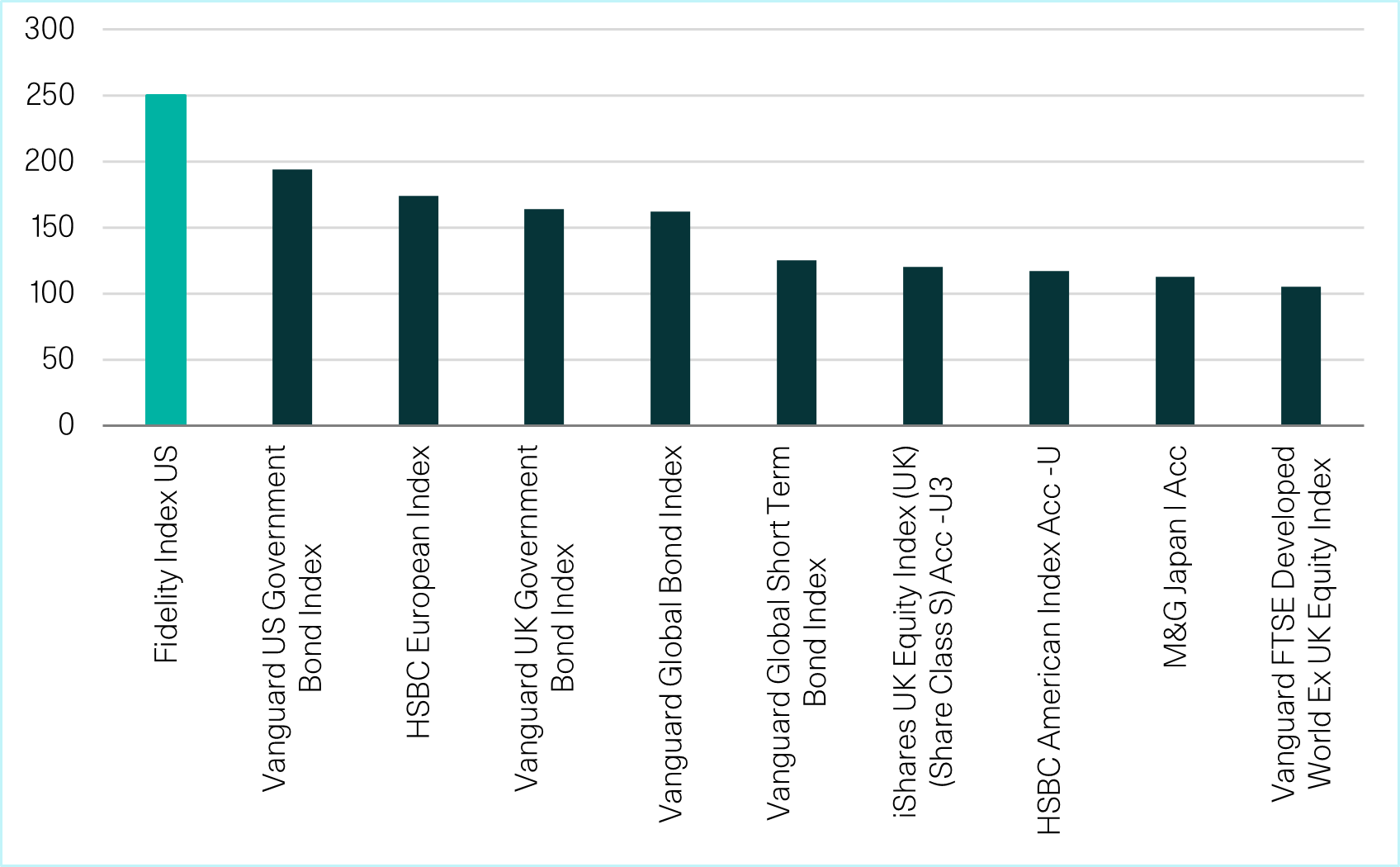

Number of MPS portfolios with similar holdings

Source: Citywire MPS Monitor, W1M. Data as at 31.12.2025.

Industry data reinforces this trend, with Morningstar stating ‘the proportion of offerings with primarily active holdings is in steady decline. Cost considerations are a key driver of the trend’. While this statement is in reference to the greater number of portfolios styling themselves as passive or blended, there is a growing proportion of portfolios labelled “active” but incorporating index funds, suggesting the number of truly active strategies is lower than one might think.

Operating under Consumer Duty, this raises an important question: does a panel of superficially different providers genuinely deliver diversification for clients, or simply replicate the same market exposures with different brands and marginally different price points?

The risk of actively-badged but passively implemented portfolios

The growing use of passive instruments inside active propositions reflects commercial pressure on fees. This is not inherently problematic. Passive investing has clear cost advantages. However, it does create the potential for unintended concentration risk across client portfolios if adviser panels lack genuine differentiation.

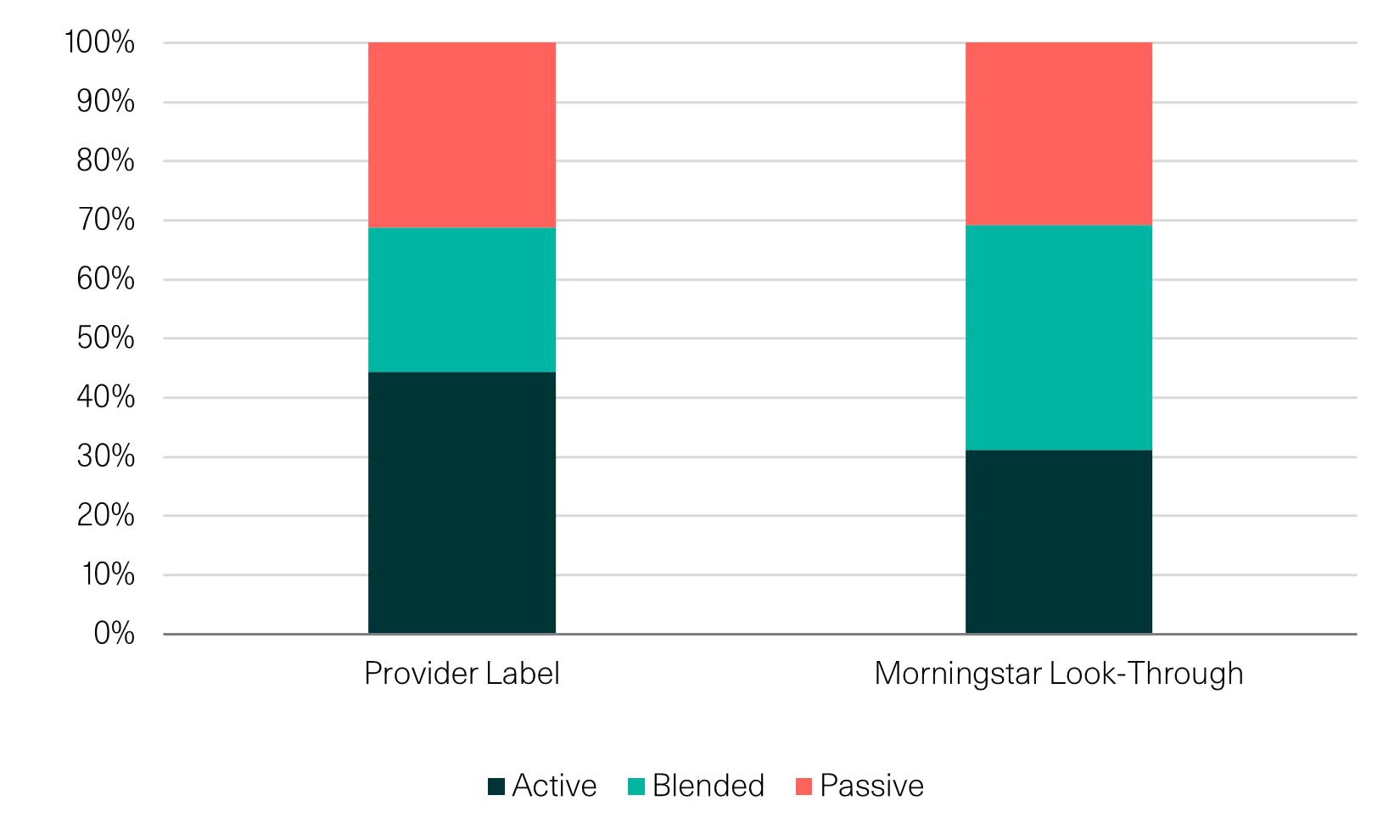

Investment style: Provider description vs. Morningstar look through analysis

Source: Morningstar Direct, author’s calculations. Data as of Sept. 30, 2025.

A differentiated approach

Against this backdrop, W1Ms MPS, built on global opportunity sets, fully active decision making and direct investment can provide a meaningful counterbalance. W1M’s portfolios are constructed using proprietary building block funds that enable direct ownership rather than outsourcing responsibility to third party managers or index trackers. This structure offers clarity over underlying exposures, known risks and expected behaviour across market environments.

Importantly, it also facilitates allocations to alternatives, particularly real assets, which can be harder to access through traditional portfolios of funds and may represent an additional source of diversification and return.

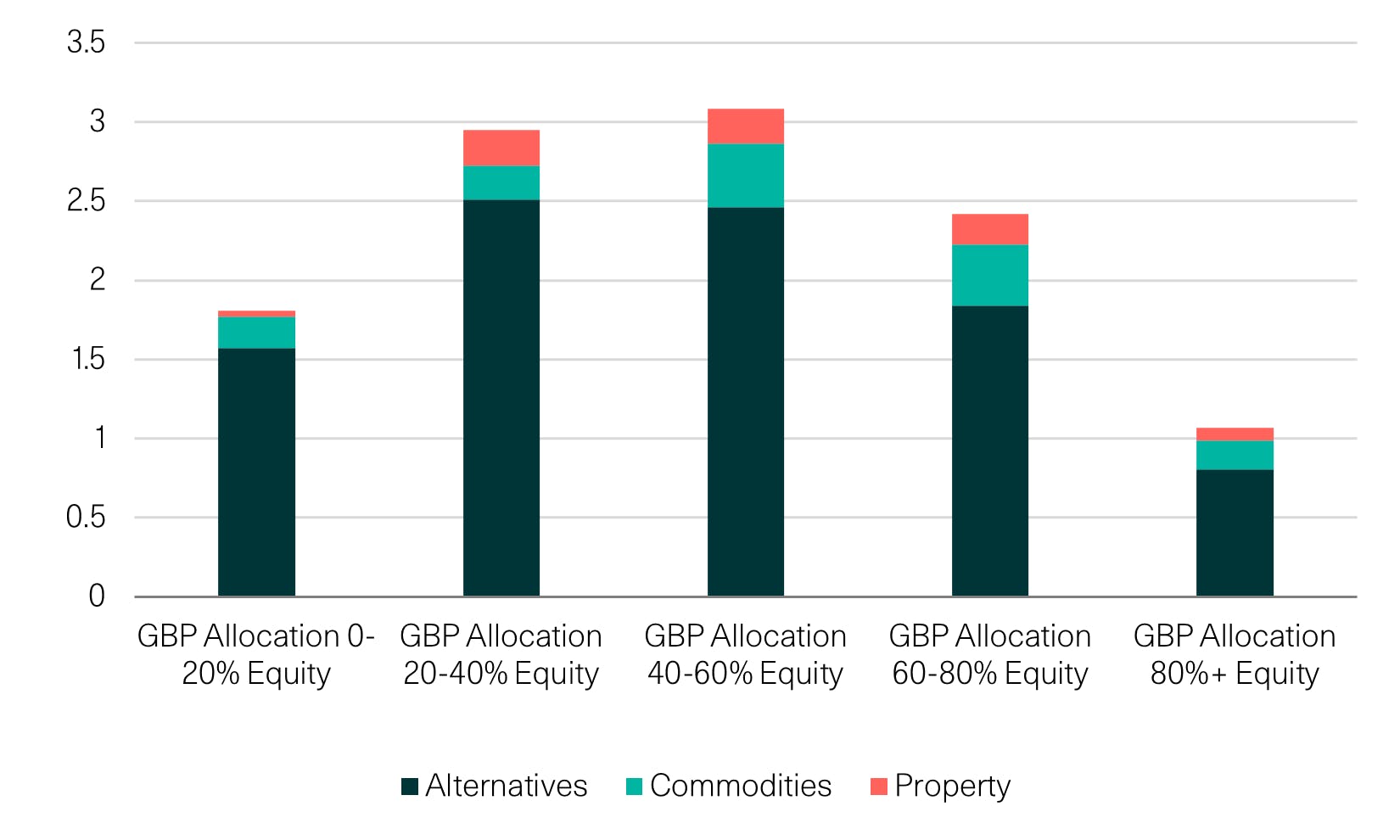

Average allocation to alternatives, property and commodities

Source: Morningstar Direct. W1M. Data as of Sept. 30, 2025.

Diversification as a Consumer Duty imperative

Consumer Duty challenges advisers not only to demonstrate value but to evidence robust manager selection. In a market where asset allocations are converging and passive usage is rising, true diversification increasingly depends on combining complementary investment philosophies rather than selecting variations of the same approach.

For adviser firms reviewing their MPS panel, the objective should be clear: avoid homogeneity, prioritise genuine active differentiation where appropriate, and ensure client portfolios are resilient across market cycles.

Ultimately, the Consumer Duty asks advisers to look beyond labels and focus on whether client outcomes truly reflect fair value, transparency and meaningful diversification. In a market where many portfolios appear different on the surface yet share similar underlying exposures, selecting genuinely distinct approaches has become essential rather than optional. This is where W1M’s position stands apart, combining a direct investment approach with active management and use of alternatives to create portfolios that are designed to behave differently across market conditions. By bringing together clarity of ownership, accountability and access to a broader opportunity set, advisers can build panels that not only meet the expectations set out at the start of this discussion but also deliver genuine diversification that supports clients over the long term.

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may rise as well as fall, and investors may not get back the amount originally invested. Capital security is not guaranteed.

This material is provided for informational purposes only and does not constitute investment advice or a recommendation. It should not be considered an offer to buy or sell any financial instrument or security. Any investment should be made based on a full understanding of the relevant documentation, including a private placement memorandum or offering documents where applicable.