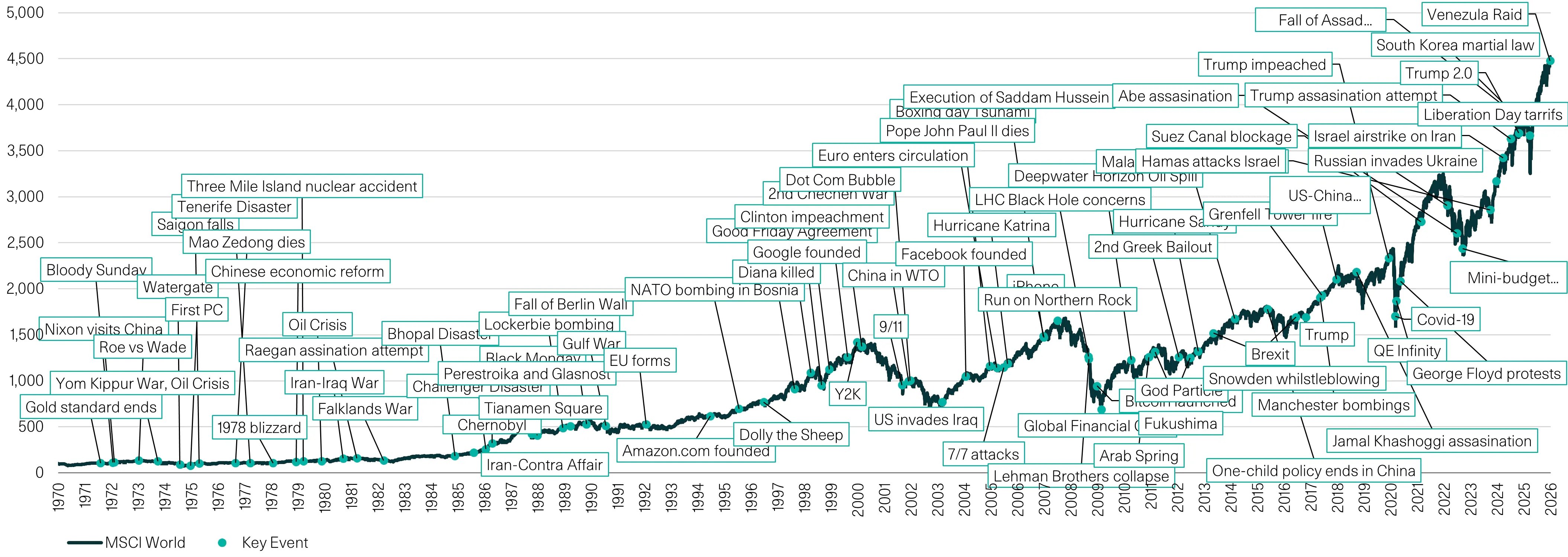

Climbing the wall of worry

Nobody knows exactly how the conflict with Iran will pan out. Things may well get much worse or victory may be declared soon and some sort of normalisation may begin. There is little point in speculating. What can investors and advisers do? For the medium to long term investor, when uncertainty is high, historically it has been right not to be driven by the relentless news cycle and emotions, but to be in properly diversified investments and patient. Let’s avoid quoting Mr Buffet but he is, of course, right that in the long run, avoiding panicking is important and panics can give opportunities. The medium to long-term investor has been rewarded historically by keeping their nerve and benefiting from continuing to add to chosen investments at lower prices during panics. “Averaging-in” in market panics can be a meaningful benefit for the investor with time on their side.

There's always a reason not to be invested...

"Climbing the wall of worry"

Source: Waverton, Bloomberg. As at 26.01.26.

Risk warning: Past performance is no guarantee of future results and the value and income from such investments and their strategies may fall as well as rise. You may not get back your initial investment. Capital security is not guaranteed.

Human beings can easily get fearful, sell up and hold cash - only to buy back into equities at higher levels.

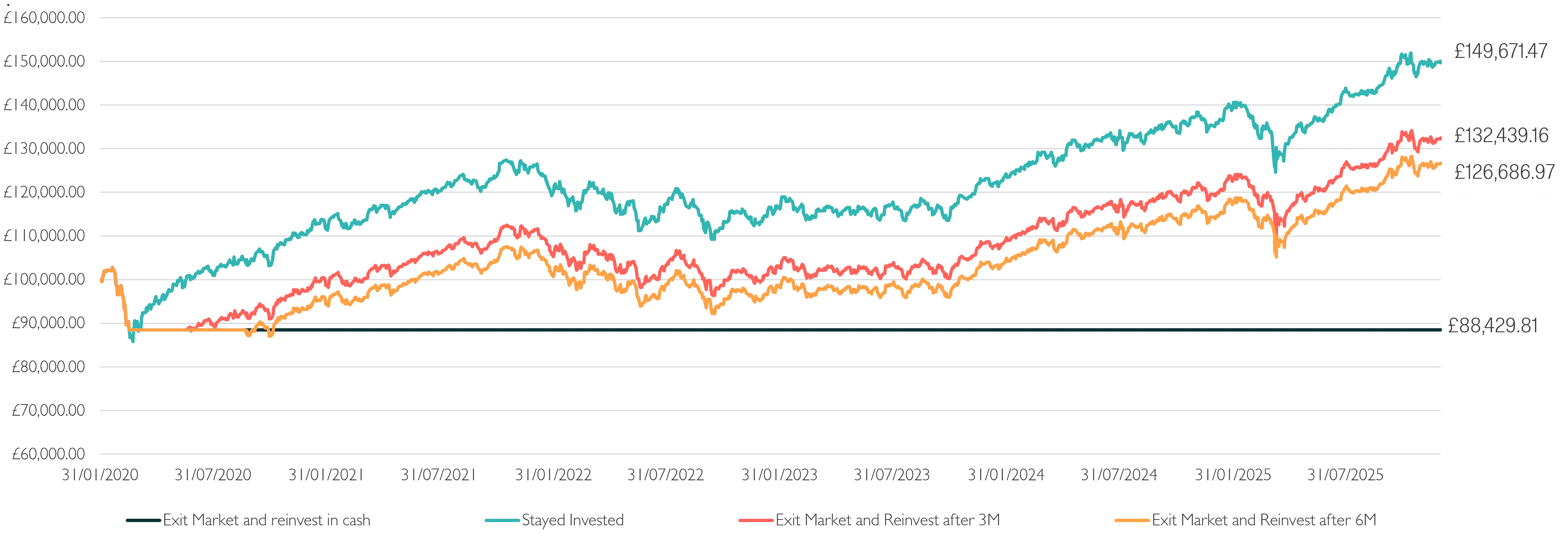

This does not seem to be a great strategy. The chart below shows that selling up in the 2020 crash and holding cash leaves people still underwater today when those who stayed invested did best. Nobody can time markets perfectly; most cannot even do it well?

Staying the course

It's about time in the market, not timing the market

What if you invested £100,000 just before the 2020 selloff?

Source: Waverton. Portfolio shown is W1M Balanced MPS on Platform. Data as at 31.12.25.

Risk warning: Past performance is no guarantee of future results and the value of such investments and their strategies may fall as well as rise, you may not get back your initial investment, capital security is not guaranteed.

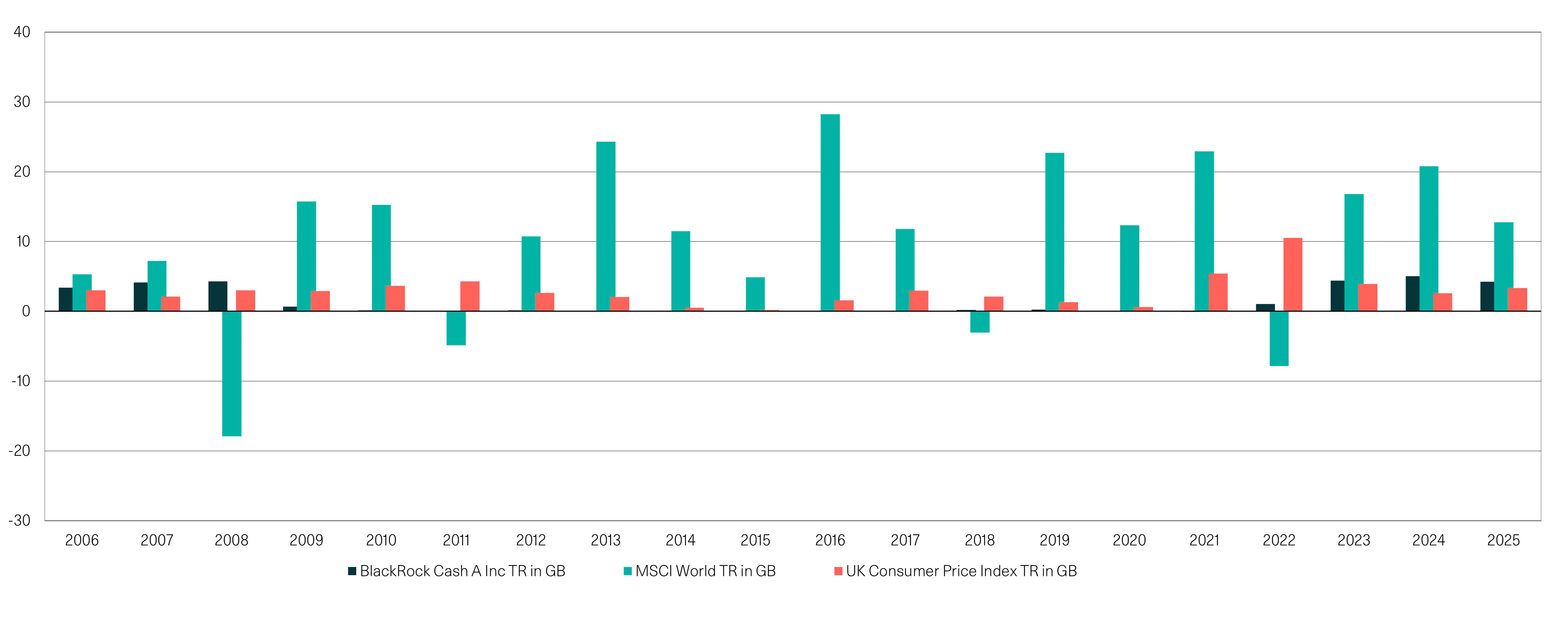

When the market is worrying about inflation or stagflation, don’t sell and hold assets which are ravaged by inflation… make sure you have inflation resilience

Stay in cash and you'll guarantee a loss of purchase power

Global equities versus cash and inflation

Source: FE fundinfo. As at 31.12.25.

Energy price shocks can lead to inflation or, even worse, stagflation when growth is weak and interest rates are going up. Investors need to diversify properly to make sure portfolios have inflation resilience.

Fixed income clearly is negatively impacted by inflation. Cash loses purchasing power as prices rise. Equities tend not to like inflation pushing up interest rates but active investors have the opportunity to buy shares in companies which have stronger purchasing power and to avoid those which are likely to be most damaged by inflation. Multi asset funds also should benefit from real assets exposures improving the inflation resilience of the whole portfolio.

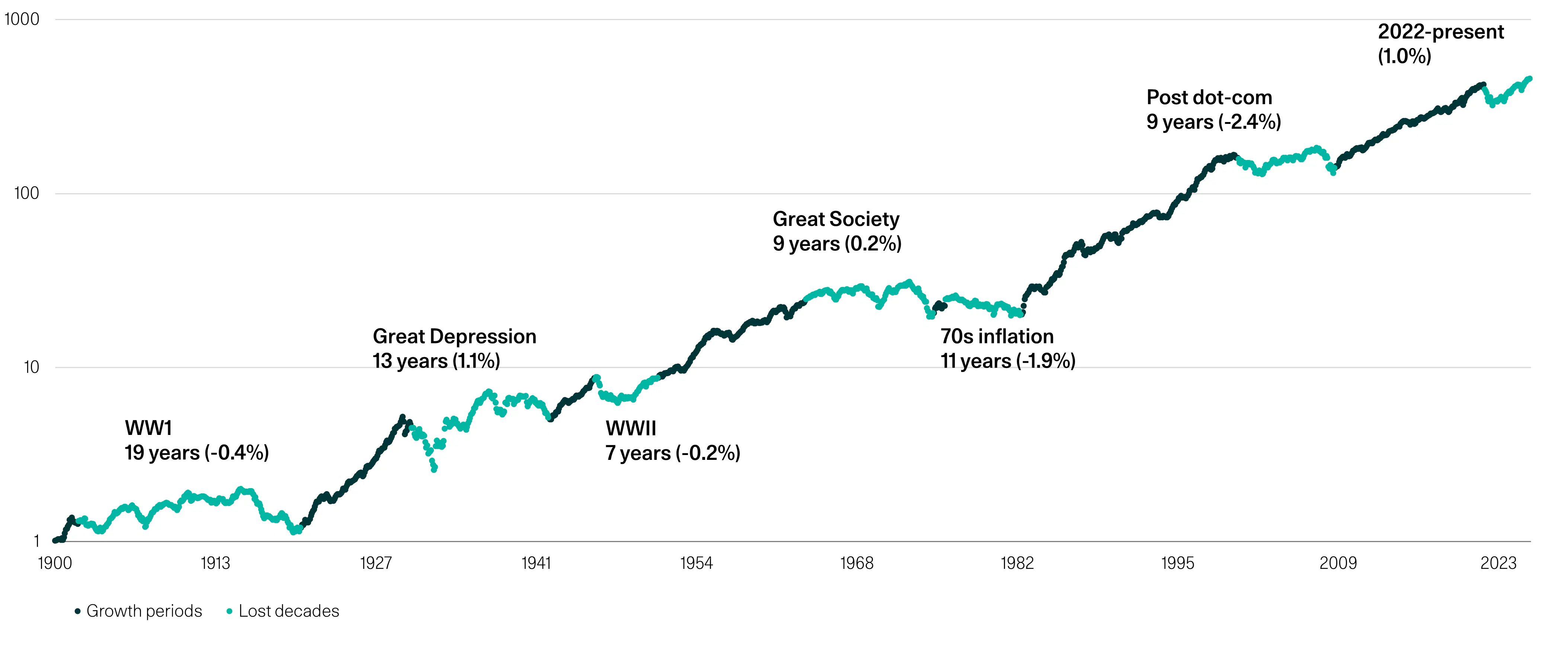

Be Active: Staying Invested does not mean just be passive

Inflation and stagflation can be very damaging to both equities and bonds; just staying invested could lead to long periods of negative real returns.

Passive 60/40 portfolios have endures 6 "lost decades" since 1900; could we be entering no.7?

Source: BofA, Bloomberg. As at 31.12.25. Note: 60/40 = 60% S&P 500 real total return and 40% US 10-year bond real total return

Risk warning: Past performance is no guarantee of future results.

Active investors can take action to mitigate emerging risks, as can be seen in our recent Multi Asset Income Fund changes.

How is W1M Navigating the Markets?

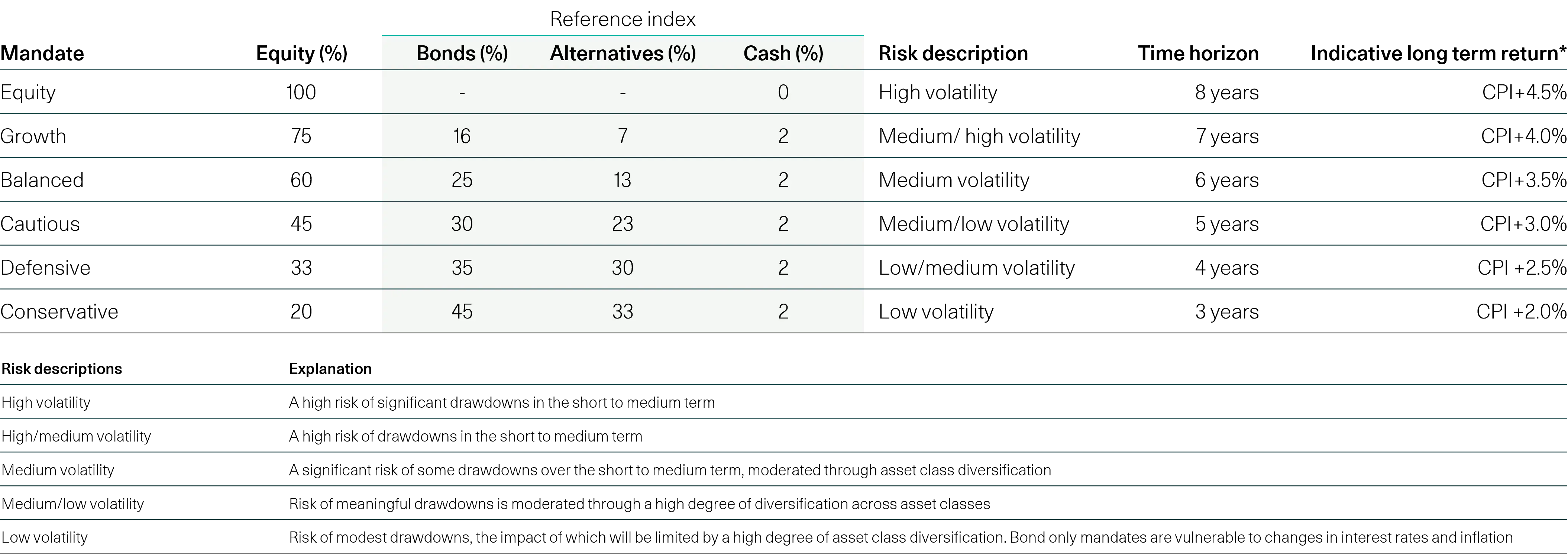

As mentioned above, keeping a proper perspective regarding time horizons is important. Our starting point is to think about what different mixes of assets are likely to achieve over defined time periods (as below). In addition to that, our aim over those periods is not linked to market indices but to beating inflation. These two elements (CPI+, clarity on time horizons) are key to how we navigate markets. We are aiming for consistent risk-adjusted returns over the medium to longer-term. Volatility in the short-term is not uncommon but less important than medium to long run delivery.

Multi-Asset: W1M Mandates

Reference £ index:

Equities: MSCI AC World Index

Fixed Income: ICE BofA UK Gilt Index | ICE BofA Sterling Corporate Index

Alternatives: S&P Real Assets Index (Hedged) | Absolute Return Index**

Cash: ICE GBP SONIA 1 Month.

*Given the unprecedented interest rate and monetary policy environment, the range of outcomes is likely to be high.

**Absolute Return Index: 66.6% HFRX Global Hedge Fund Index, 33.3% ICE BofA 1-3 Year UK Broad Market Index

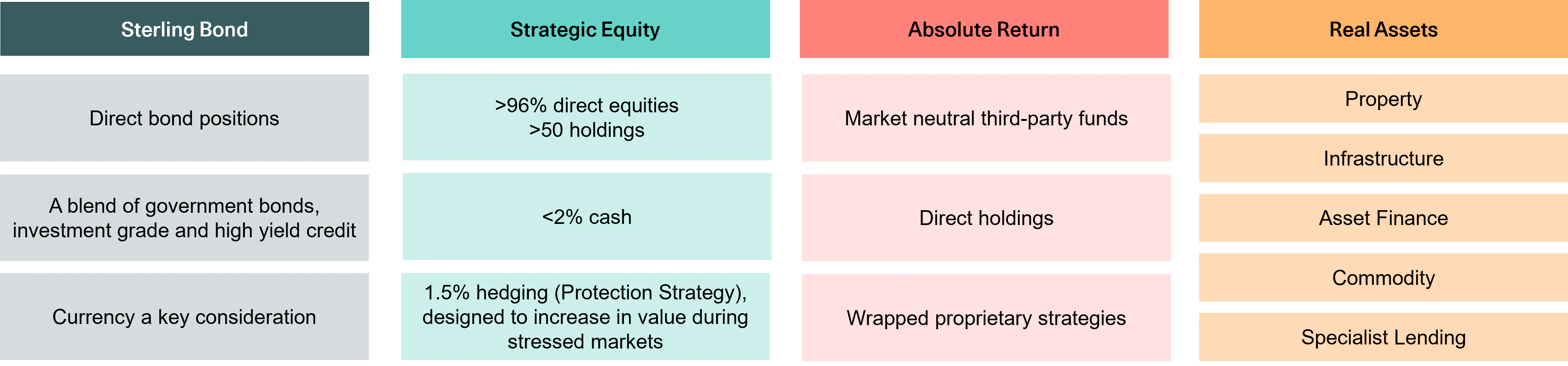

Active in Equities, Fixed Income, Real Assets and Absolute Return Strategies

W1M does not own every stock in the major indices but actively chooses around 50 stocks for most portfolios; when inflation means pricing power matters even more than usual for companies, we want to be active in stock selection. Similarly, in fixed income, we are active, with a preference for gilts relative to credit, but underweight the asset class overall. Absolute Return and Real Assets exposures improve the risk adjusted return characteristics of portfolios and add to inflation resilience.

Be efficient and properly diversified in portfolio construction

Tax-efficient wrappers that have been specifically created for the purposes of these portfolios

- Swift, efficient and consistent trade execution

- Access to funds and structures that would not otherwise be available

- Underlying funds accessed at institutional rates or better

- CGT and VAT benefits to structure

Risk warning: The tax treatment of investments depends on each investor’s individual circumstances and is subject to changes in tax legislation.

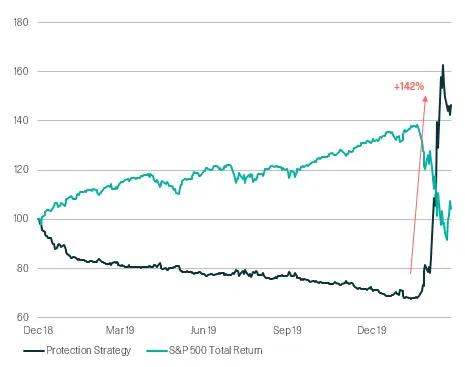

Protection Strategies are integrated into W1M portfolios

If markets get extremely volatile, we have, in effect, “taken out some insurance”. If nervousness increases and volatility spikes, our protection strategies can have significant gains just when other assets may be falling sharply. Having exposures in portfolios which are uncorrelated with equities, in particular, is helpful both in terms of managing risk and delivering returns over the longer term.

Actual PS performance vs S&P 500 (TR)

How did it perform during Covid-19 crisis

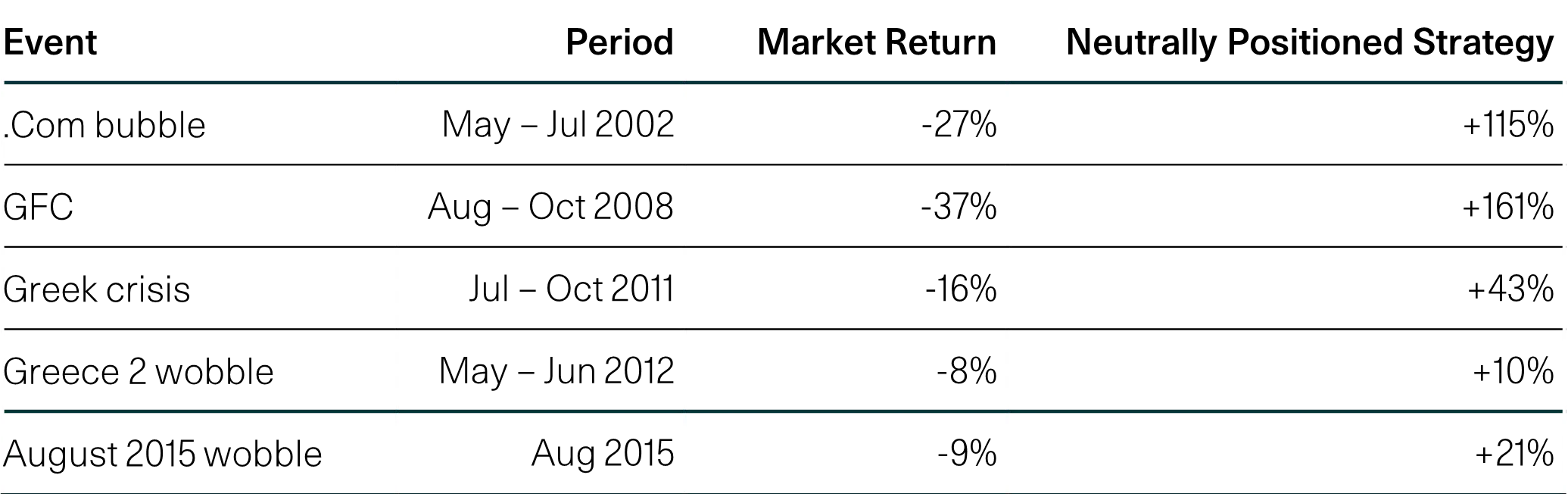

Back-tested returns in previous crises

*Inception: 19th April 2016 Data to from 31.12.19 to 31.03.20

Source: Goldman Sachs, Bloomberg, W1M.

Figures are calculated on a total return basis, net of fees.

Risk Warning: Past performance and simulated past performance is no guarantee of future results and the value of such investments and their strategies may fall as well as rise. You may not get back your initial investment. Capital security is not guaranteed.

Summary of our views

While markets are volatile, the key thing is to assess is whether medium and longer-term prospects are being damaged or not. The longer conflict with Iran continues, the more risk there is to the medium-term global growth and inflation picture. Market consensus is being tested today but has been expecting that finding an “off ramp” to end the war is in US, Iranian, Middle Eastern, Chinese and nearly all global interests. Clearly, events can change economic prospects significantly and it is key for investors to be properly diversified but also active in the current environment.

Energy prices spiking and greater inflation risk mean we remain underweight fixed income, but retain a preference, within it for UK government bonds (gilts) relative to corporate debt. Owning every stock in the major indices, regardless of valuations, is not necessarily a good strategy, especially when some stocks are pricing in incredible growth and are sensitive to interest rate expectations; we remain convinced it is right to be active in an environment where a small number of stocks now represent a significant part of the total market and when geopolitical risks persist. We are neutral on equities at the portfolio level but still find good ideas globally, thinking about medium to longer term prospects. Real assets offer diversification and inflation resilience which are now more needed as a result of geopolitical events. Proprietary protection strategies are a valuable and distinctive component of our portfolios in an uncertain world.

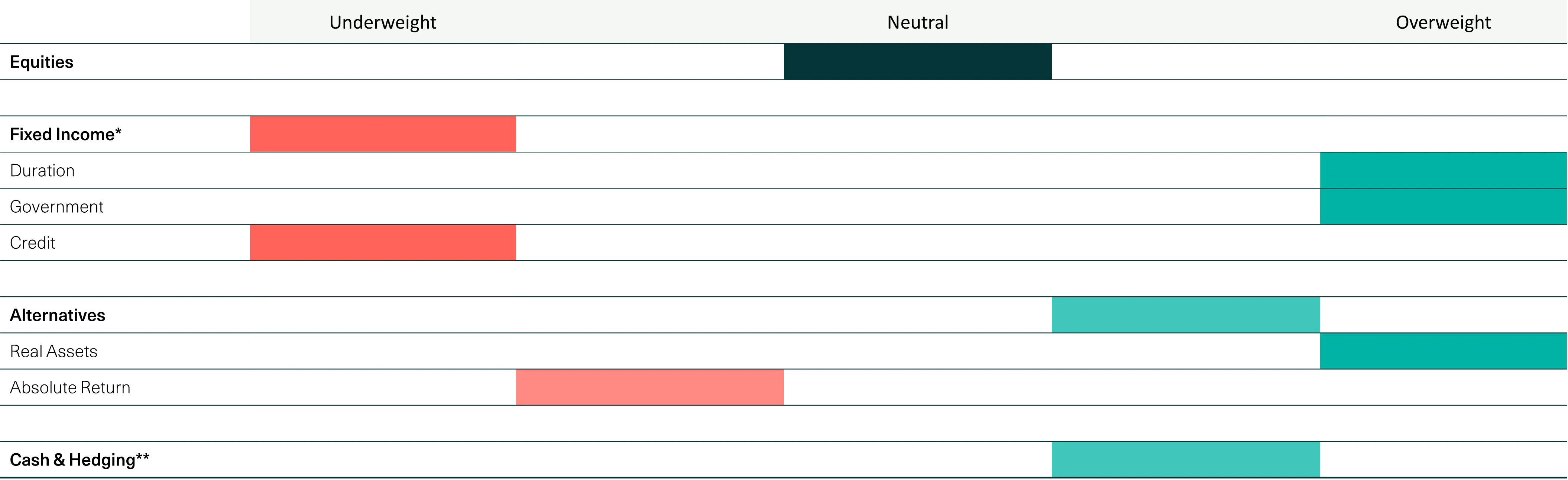

March 2026 Asset Allocation positioning

*The table shows bond allocations relative to bond composite index

**Hedging includes gold & Protection Strategy if possible.

Source: Morningstar. As at 05.03.26. The weightings are calculated as a percentage of the Waverton Balanced platform model portfolio and the peer group equivalent of Model GBP Allocation 40-60%. MSCI AC World weighting assumes a 60% allocation to equity. The above should be used as a guide only and is subject to change.

Past performance is not a reliable indicator of future results. The value of investments and the income derived from them may rise as well as fall, and investors may not get back the amount originally invested. Capital security is not guaranteed.

This material is provided for informational purposes only and does not constitute investment advice or a recommendation. It should not be considered an offer to buy or sell any financial instrument or security. Any investment should be made based on a full understanding of the relevant documentation, including a private placement memorandum or offering documents where applicable. W1M Wealth Management Limited is authorised and regulated by both by the Financial Conduct Authority of 12 Endeavour Square, London E20 1JN, with firm reference number 120776 and the U.S. Securities and Exchange Commission of 100 F Street, NE Washington, DC 20549, with firm reference number 801-63787. Registered in England and Wales, Company Number 02080604.

All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without prior written permission from W1M Wealth Management Limited.

Copyright © 2026 W1M Wealth Management Limited.